Celsius Network was never a real business. It did not have a viable business model. Really, it was a momentum trading scheme that relied on the premise that crypto prices would always rise. And when they didn't, it resorted to fake valuations and market manipulation to escape insolvency. It was fraudulent from the start.

This is the conclusion I've reached after studying

the U.S. Examiner's final report (yes, I've read all 476 pages of it) and Celsius's audited reports and accounts up to 31st December 2020. There are no more recent audited accounts. It was due to file its 2021 accounts by 31st December 2022, but it did not do so. The accounts are now significantly overdue. I doubt if they will ever be filed.

The U.S. Examiner's report reveals deep and long-lasting insolvency, concealed by layer on layer of fraud. Whether Alex Mashinsky, Celsius's founder, owner and CEO, knew that the devices he used to conceal the company's insolvency were fraudulent is uncertain. But I am certain that whoever was advising him knew. Mashinsky's associates are, understandably, portraying him as a loose cannon who made all the operating decisions and wouldn't listen to advice, and no doubt this is to some degree true. But some of the concealment schemes were devised by a financial expert. Mashinsky doesn't have that sort of expertise. This fraud was a team effort.

Loans for shares

One of Celsius's elaborate concealment schemes arose from an attempt to raise market funding to develop its business. In March 2018, Celsius did an Initial Coin Offering (ICO) in which it offered 325 million CEL tokens for sale to the public. Prices ranged from $0.20 in the private pre-sale to $0.30 during the sale period itself, with bonus schemes reducing the effective price in many cases.

Had Celsius sold all 325m tokens, it would have raised some $50m. But the ICO flopped. Celsius only managed to sell 203m tokens, and raised only $32m. Nevertheless, it proceeded as if the ICO had been fully subscribed. On 18th April 2018, Celsius minted 700m CEL tokens and distributed 203m of them to purchasers. It retained 325m as "Treasury stock", and placed 50m in a smart contract which would automatically release them if the price of CEL hit certain benchmarks. The remaining unsold tokens should have been burned - but only a few of them were.

Mashinsky's company A.M. Ventures (AMV) agreed to purchase any unsold tokens from the ICO at $0.20, up to a maximum of $18m, plus a 30% bonus. So, after the ICO failed, AMV bought 117m tokens for $18m. But it did not complete the purchase. The 117m tokens were left in limbo. They were "owned" by AMV, but "custodied" by Celsius. Obviously, Celsius couldn't burn them. So it segregated them in a separate blockchain wallet.

But neither Celsius nor AMV could profit from the tokens. They were stuck in limbo. So between them, the two companies devised an elaborate scheme to transfer them to Celsius's balance sheet. The U.S. Examiner describes it thus:

"In January 2020, Celsius and AM Venture attempted to paper over AM

Venture’s failure to close on its purchase agreement by entering into a loan

agreement. Under the loan agreement, AM Venture would borrow $18 million

from Celsius at 6% annual interest. AM Venture would then allow Celsius to

offset AM Venture’s obligation to purchase $18 million worth of CEL To

secure the loan, AM Venture would pledge the 117 million in CEL that AM

Venture had agreed to, but did not purchase, and Mr. Mashinsky would pledge

his stock in Celsius Network Inc."

Now, on the surface this appears straightforward, if expensive. AMV sold the tokens back to Celsius at a significant premium over what it paid for them, the difference to be paid in instalments, with the premium partially discounted by equity shares in Celsius. (14th February 2023: paragraph amended to correct the direction of the interest payment)

But AMV hadn't completed its purchase of the CEL tokens. It didn't own them. So it couldn't "pledge" (or sell) them to Celsius. Furthermore, since Mashinsky owned both companies, Celsius's equity pledge was meaningless. So what was really going on?

Taking the tokens out of the picture reveals a fraudulent self-financing scheme. In Celsius-speak, "pledge" means full transfer of ownership rights for a period of time. So Celsius actually lent $18m to AMV to purchase its own share capital. Lending to purchase own shares is illegal in most jurisdictions. Moreover, since Mashinsky owned both companies, he was pledging shares he already owned to himself, presumably to give the impression that this was a legitimate market transaction. It was a clever deception devised by someone well-versed in corporate finance and accounting.

Celsius's management knew this scheme was fraudulent. One senior manager, Ashley Harrell, commented that AMV couldn't pledge tokens it didn't own. But it didn't last long. A few months later, Celsius and AMV wrote off the loans. And in December 2020, Celsius took the 117m tokens onto its own balance sheet, inflating its value by $628m. I'm pretty sure this was the end goal of the scheme.

The amazing balance sheet inflation scheme

The "loans for shares" scheme was far from the first time Celsius's management had used CEL tokens to inflate its balance sheet. In fact it did so from the moment they were issued. Without them, Celsius would have failed in its first year of trading.

The accounting policies in Celsius's first set of audited accounts, made up to 28th February 2019, reveal that it held the 325m CEL tokens in its Treasury at fair value, with changes in value taken to P&L through "other comprehensive income". Furthermore, although the tokens were minted within the accounting period, it did not record any production costs for them (my emphasis):

"The company considers that treasury cryptocurrencies are an intangible asset with an indefinite useful life as the Company considers that they do not have an expiry date nor have a foreseeable limit to the period of which they will be exchanged with a willing counterparty for cash or goods and services. Treasury cryptocurrencies relate to CEL tokens held by the company and can be issued at the company's discretion. No costs were capitalised in respect of treasury tokens in line with the company's policy on research and development.

So although the individual CEL tokens were individually worth very little, 325m of them recorded at fair value and zero cost was a substantial boost to Celsius's balance sheet. We don't know how they determined the fair value of the tokens, but a back-of-the-envelope calculation using Coingecko's CEL price on 28th February 2019 gives a value of approximately $12.8m, all of which was taken to P&L. It is included in the "Other Comprehensive Income" line in the income statement:

Clearly, the fair value of Treasury CEL tokens was significantly more than the amount booked to other comprehensive income. But Celsius was also holding other crypto assets at fair value - and this was the "crypto winter" of 2018-19, during which the prices of crypto assets fell considerably. Bitcoin's price, for example, fell from nearly $20,000 in December 2017 to less than $3,000 by the end of February 2019. So Celsius was taking heavy losses on the fair value of its other crypto assets. Deducting the $12.8m I have estimated as the fair value of Treasury CEL tokens at that time turns a revaluation surplus of $8.7m into a loss of around $4.1m. Adding this to the headline loss for the period of nearly $1.5m gives a total comprehensive loss for the period of approximately $7.2m.

On the balance sheet, Celsius recorded intangible assets of $51.67m:

But this includes the Treasury CEL tokens. Deducting their estimated value of $12.8m reduces Celsius's intangible assets to $38.87m, and its net assets to negative $7,244, wiping out its entire shareholders' equity.

So Celsius was insolvent in its first year of trading. It should have gone into bankruptcy in the UK. But by recording its own issued tokens at fair value on its balance sheet and taking this into P&L as unrealised gains, it convinced its auditors, Companies House and the general public that it was a going concern. What a racket.

To be fair, at the time that these accounts were produced - and indeed still today - there were no generally-accepted accounting standards even for cryptocurrencies such as Bitcoin, let alone for own tokens. So Celsius didn't break any rules by inflating its balance sheet in this way. But concealing insolvency is at best misleading and can be actually fraudulent. And it did not wholly escape the notice of the auditors.

The Notes to the Accounts recorded a warning that the company might not be able to continue as a going concern, ostensibly due to the threat of Covid. As these accounts are supposedly made up to 28th February 2019, which was best part of a year before the threat of Covid even emerged, this is not a credible reason for the going concern warning. However, the auditors noted it:

"We draw attention to note 2.2 in the financial statements, which indicates that while the directors consider that the company has adequate resources to continue in operational existence for the foreseeable future, there is uncertainty due to the impact of the COVID-19 virus which cannot yet be fully quantified. As stated in note 2.2, these events or conditions, along with the other matters as set forth in note 2.2, indicate that a material uncertainty exists that may cast significant doube on the Company's ability to continue as a going concern."

And to cover their own backs, they included a disclaimer placing all responsibility for any fraudulent misrepresentation on Celsius's directors:

"Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an Auditor's Report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs (UK) will always detect a material misstatement when it exists. Misstatementss can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements".

This is probably a standard disclaimer, but.... no, I reckon they knew the company was insolvent.

The cash haemorrage

A year later, Celsius was in even deeper trouble. Its accounts dated 28th February 2020 reveal a company teetering on the edge of bankruptcy. It posted a whopping before-tax loss of nearly $40m, and an operating loss of some $28m, largely because of a toxic combination of falling turnover and rapidly rising cost of sales:

Once agin, revaluation of intangible assets came to the rescue. A whopping loss magically became total comprehensive income of $28.65m. Partly, this was because of a general rise in crypto prices over the course of the year, which resulted in significant fair value gains on Celsius's crypto asset holdings. But it was also helped by the increase in value of the CEL token during that time. Using the same method as I used above, I calculate that the total value of the Treasury CEL tokens had risen from $12.8m to approximately $47.6m. Deducting the fair value gain of $29.8m on these tokens from Other Comprehensive Income reveals a total comprehensive loss of approximately $1.5m.

Now, I know you're thinking "that's not too bad". True, it's not. But Celsius's actual business was losing money hand over fist. And the cash flow statement shows that it was also bleeding cash. Between March 2019 to February 2020 it suffered a net operating cash outflow of $25.4m and spent nearly $50m buying "short term unlisted instruments". It financed this cash drain with new borrowing totalling nearly $87.6m. The additional borrowing meant it ended the year with a positive cash balance, but at the price of a massive increase in debt. By the year end its short-term borrowing (less than 1 year) totalled over half a billion dollars, and its current ratio - a crucial measure of liquidity - was flashing red at only 0.6. Celsius was dreadfully short of cash and in serious danger of not being able to meet its obligations.

As in the 2018-19 accounts, the notes to the 2019-20 accounts contain a warning that Celsius might not be able to continue as a going concern. Again, Covid is blamed, and with some justification this time, since the pandemic struck the UK with full force in March 2020, forcing the government to impose a lockdown that remained in place with varying degrees of strictness for the next two years. But my analysis shows that the company would have gone down anyway - unless it found a means of generating cash.

The flywheel

The crypto world doesn't have any endogenous sources of cash. Crypto lenders like Celsius can't create dollars when they lend in the way that banks do, and they can't tap the Fed for liquidity. They can borrow from banks and financial markets if they have acceptable collateral, but crypto assets generally aren't acceptable. So for a cash-strapped lender like Celsius, there are really only two sources of dollar liquidity: investors, and depositors. Celsius went for both.

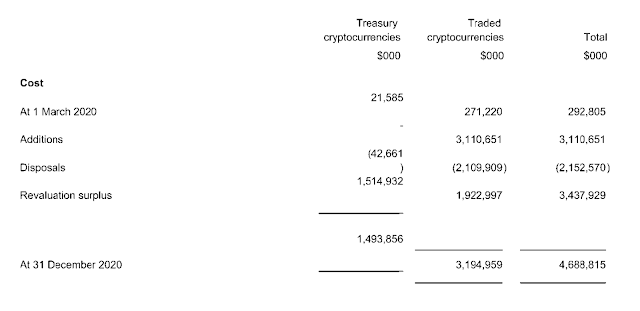

In 2020, Celsius changed its year-end to December. So the final set of accounts it produced while headquartered in the UK covers the period from 1st March 2020 to 31st December 2020. And it documents a remarkable transformation in Celsius's fortunes. In ten months, it moved from a fragile small company bleeding cash at an unsustainable rate to a cash-generating behemoth. The "going concern" warning disappeared from its accounts, though the auditors still warned (presciently, as it turned out) about the possibility of fraudulent misstatement.

But a closer look reveals that the underlying fragilities were still there. In fact they were much, much worse. During the period, Celsius sold some shares, raising $23.26m of unencumbered dollars. But the rest of the money it managed to attract came from short-term creditors, principally new depositors. In ten months, current liabilities rose from $0.5 billion to $4.8 billion, of which $3.9 billion were new deposits.

As a result of this influx of new money, Celsius's end of year cash postion improved to $17.8 million, and its total current assets increased to $2.203 billion. But its liquidity had actually deteriorated. Its net current liabilities were $2.6 billion and its current ratio had slipped to 0.39. It had no means of repaying its short-term creditors.

What was it spending the money on? Mainly, buying and selling cryptocurrencies. During the period, it bought $3.1bn and sold $2.15 bn, and at the end of the period it recorded a revaluation gain of $1.51 bn.

Without this gain, Celsius would have once again been in balance sheet insolvency at the end of the period.

We now know that the cryptocurrency Celsius was so actively trading was is own token, CEL. By the end of 2020, the "fair value" of Celsius's Treasury CEL tokens had risen from a few millions to $1.5bn. Once again, Celsius had escaped insolvency by puffing up its balance sheet with its own tokens.

But this time, the fair value gain did not arise from Celsius's accounting policies and the absence of generally-accepted accounting standards for crypto assets. The U.S. Examiner explains how from May 2020, Celsius's business strategy changed from simple deposit-taking and lending to actively manipulating the price of CEL:

"In May 2020, Celsius’s strategy became more nuanced. In connection with

discussions of overall strategy for buying CEL, Mr. Mashinsky stated his basic

premise: “Our job is to protect CEL . . . .” In line with this thinking, the new

approach to CEL management had one “main thesis”—that Celsius will “rise and

fall with CEL" "

The Examiner says there were three main components to Celsius's CEL manipulation:

- Celsius began to regularly buy back more than 50% (and usually

100%) of the weekly CEL rewards from the market... Based on the setting of reward rates, Celsius would calculate how much

CEL was needed to pay customers rewards. Celsius would time its purchases of

the needed CEL throughout the week to either raise the price of CEL or avoid a

price drop. This strategy proved to be successful.

- Celsius began placing “resting orders” of CEL purchases on

exchanges at prices below the then-current market price of CEL; these resting

orders would automatically trigger if CEL dipped to the specified price. For

example, if CEL was trading at $0.10, Celsius would put in an order to

automatically purchase a specified amount of CEL at $0.08. Celsius did this for

the express purpose of token price control... To ensure that Celsius stayed ahead of market

conditions, Mr. Treutler and Mr. Nolan, and later Dean Tappen (Coin

Deployment Specialist) would monitor CEL trading activity seven days a week

and readjust the “resting orders” as needed to protect the price of CEL.

- Celsius started using its over-the-counter (OTC) trading desk to sell

CEL. These sales, which were made at market prices, went “hand in hand with

the weekly CEL purchases for Interest payments. . . .” This strategy was

internally referred to as the “OTC Flywheel” and operated on the theory that:

“[t]he more CEL we sell . . . [t]he more CEL we can repurchase . . . [t]he more

attractive CEL markets look like . . . [t]he more CEL buy orders we received . . .

[t]he more our Treasury is worth.

This chart shows the correlation between Celsius's buybacks and CEL's price.

Clearly, CEL's price was driven to a large extent by Celsius's buybacks.

Selling and buying back stocks or securities to give the impression that they are more heavily traded than is actually the case, thereby enticing other market participants to buy them and thus pushing up the price, is known as "

painting the tape". It is market abuse and is illegal in most jurisdictions, including both the U.K. and the U.S. Celsius had crossed a line.

And it had also ensured its own eventual demise. Celsius's "flywheel" was far from cost free. It increased Celsius's leverage and decreased its liquidity - hence the deteriorating current ratio. As CEL's price rose, Celsius would need more and more new funds to pay for the buybacks. It would become increasingly illiquid. Furthermore, since there is a finite number of new investors and depositors, eventually the flywheel would stop spinning. Indeed, once investors and depositors realised Celsius wasn't in a position to pay them the returns it promised - or even return their funds - the flywheel could go into reverse. If it did, the end would come quickly. Even in 2020, Celsius was so highly leveraged and illiquid that insolvency was inevitable once customers started withdrawing their money.

There's a disturbing similarity between Celsius's "flywheel" and the

unstable leveraging flow system that crashed so disastrously in 2008. Systems like these are only self-perpetuating so long as the conditions that enable them remain. What Celsius needed to keep its flywheel spinning was an ever-increasing supply of new money, coupled with control of sales (so it could keep prices rising in line with inflows of new money). If either of these failed, Celsius would be in serious trouble. As Chuck Prince, ex-CEO of Citigroup, said: "When the music stops, in terms of liquidity, things will be complicated.” For Celsius, this turned out to be an understatement.

Heavy marketing of Celsius's deposit schemes to retail customers kept the flywheel spinning for nearly two years. But Celsius never had complete control of sales. From May 2020 until its eventual collapse in July 2022, there was an active seller of CEL tokens - one Alex Mashinsky. Mashinsky is

estimated to have made $44m from sales of CEL tokens. All of these tokens were subsequently bought back by Celsius. A Celsius senior manager cited by the U.S. Examiner says that Celsius management knowingly used customers' and investors' money to fund buybacks of CEL tokens sold by Mashinsky and other insiders. That is fraud.

Evading the regulators

On 22nd June 2021, the U.K.'s Financial Conduct Authority issued a general warning about over 100 crypto companies operating in the U.K. without a licence, saying they posed a risk to the financial system and consumers, banks and payment companies should not deal with them. Celsius, it seems, was one of them. The following day, Celsius announced that it was terminating its outstanding application for an FCA licence and withdrawing from the United Kingdom. Its new headquarters would be in Delaware, U.S.

But in fact, its U.K. entity remained active. Indeed, rather a lot of Celsius's subsequent business was channelled through it. In important respects, such as the location of corporate and customer assets, Celsius remained a U.K. company. It merely transferred to Delaware its retail customer -facing business. We now know that it did so not because of "regulatory uncertainty", as it claimed in its

community update, but to avoid being closed down by the FCA. On 11th June 2021, the FCA notified Celsius that its business constituted an unregulated collective investment scheme (UCIS) under the Financial Services and Markets Act 2000, which, since 2013,

cannot legally be sold to ordinary retail customers.* It ordered Celsius to cease selling to retail customers in the U.K. and withdraw its application for an FCA licence.

It is unfortunate that the FCA's action merely encouraged Celsius to relocate in a different country. Had the FCA closed Celsius down at this point, much pain and loss would have been spared.

To comply with the FCA's order, Celsius transferred all customer obligations to the U.S. entity and ended deposit-taking in the U.K. But its institutional lending and treasury management, including deployment of CEL tokens, remained in the U.K. entity. To conceal the glaring mismatch between assets and liabilities that this created, the lending-related assets retained in the U.K. entity were recorded as a demand loan from the U.S. entity. This made the U.K. entity the lending agent of the U.S. entity in much the same way as

Alameda was the lending agent for FTX. The U.S entity trawled for retail deposits and fed them to the U.K. entity, which lent them out for a return.

So Celsius's business was split between two countries. The deposit-taking engine that drove the flywheel was in the U.S.; but the lending that generated the returns promised to depositors, along with the CEL token purchases, sales and burns that stabilised the flywheel, were in the U.K. Neither the U.S. nor the U.K. company stood alone as an independent company.

But internally, Celsius's management accounting didn't distinguish between them. To Celsius's management, there was only one business, and the fact that it was split between the U.S. and the U.K. was merely an inconvenient device to evade the FCA.

The U.S. Examiner's disclosure that the U.S. company was "insolvent from inception" appears shocking, but is really of interest only as evidence of the lengths to which Celsius would go to escape the attention of regulators.

Of much more importance is the long-standing insolvency of the entire Celsius Network and the fraudulent devices Celsius used to conceal it. And so I move on to the fundamental issue underlying all of this.

Why was Celsius never a viable business?

Celsius's primary business was deposit-taking and lending. Indeed, to start with, this was its sole business. This is its purpose as stated its 2018/19 report and accounts:

"Celsius Network Limited ("the Company") was created to create a community centric organization that will always act in the vest interest of its customers and depositors, providing two services:

1. The ability to deposit digital assets and earn yield on such assets

2. The ability to borrow or take a loan against such assets"

Deposit-taking and lending is the business of banking. Celsius was an unregistered, unregulated bank - what we know as a "shadow" bank. Shadow banking is usually a profitable business, sometimes exorbitantly so. Admittedly, shadow banks tend to implode disastrously when economic conditions turn against them, and Celsius certainly was no exception. But Celsius seems to have been totally unable to profit from its core business even in the good times. It reported headline losses year after year, and relied on inflating the value of its own tokens to escape the bankruptcy court. Its core business was simply never viable. Why was this?

The problem was the return Celsius promised to its depositors. Banking is a margin business: to be profitable, a bank must earn more money from lending than it pays to depositors. "Net interest margin" (NIM) is the difference between the average interest rate on loans and the average interest rate on deposits. The wider that margin, the more profitable the bank. If net interest margin is persistently too low to cover administrative and other expenses, the bank will be loss-making unless it can earn sufficient income from other sources (fees, for example) to cover those expenses.

Celsius's NIM was persistently too low to cover its expenses. At times, it was negative. Celsius's marketing model relied on offering depositors higher interest rates than its competitors, but it was unable to generate sufficient income from lending to pay these exorbitant returns. It also did not charge fees. In short, its pricing model was broken from the start.

In 2019 through 2021, Celsius concealed its broken pricing model by reporting significant unrealised income from fair value gains on crypto asset holdings. We now know this income was mainly from its own token, and from mid-2021 onwards was fraudulently generated. Anyway, fair value gains cannot conceal headline losses. All three annual reports filed with the U.K.'s Companies House reported substantial headline losses. And although Celsius has not filed a report for 2021, a Board presentation recorded in the U.S. Examiner's Report says it would have turned in a headline loss of $881m.

But Celsius's financial position deteriorated rapidly when crypto entered a bear market in early 2022. Despite taking ever-larger risks, it had been unable to improve its lending income sufficiently to pay its depositors. And it was no longer able to mitigate losses on its core business with unrealised gains on its CEL tokens. It didn't have sufficient liquidity to buy back the tokens in the quantities needed to support the price, so CEL's price started to fall - rapidly. This had a disastrous effect on Celsius's solvency. After all, if you mark your Treasury assets to market when their price is rising, you must also do so when it is falling. This chart shows how the carry value of Celsius's Treasury assets collapsed as CEL's price fell:

Concerned by Celsius's persistently poor NIM and growing illiquidity, some members of Celsius's senior management pushed for interest rate reductions on deposits, including CEL rewards. But they were overridden by Alex Mashinsky. Right to the end, Celsius continued to pay above-market interest rates on deposits and offer financial incentives to attract new depositors to the platform.

Celsius's death knell was sounded by the collapse of TerraLuna in May 2022. This sparked a bank run which fatally destabilised the "flywheel" and rapidly drained what was left of its liquidity. By June, Celsius was so short of money that it was using new deposits to pay the returns it had promised to existing depositors. It had become a Ponzi scheme.

The end for Celsius came quickly. On 12th June, it suspended withdrawals. And a month later, on 13th July, it filed for Chapter 11 bankruptcy.

Would Celsius have survived if crypto hadn't entered a bear market, and if TerraLuna hadn't crashed? No. It would simply have taken longer to die, and lost even more of its customers' and investors' money. Really, the events of 2022 were a kindness. The tragedy is that because accountants and regulators on both sides of the Atlantic failed to spot the red flags, this company was able to defraud people of their money for four long years.

Related reading:

Celsius Network's reports and accounts for February 2019, February 2020 and December 2020 can be downloaded from the U.K.'s

Companies House website. No published accounts exist after this date.

* The U.S. Examiner's report incorrectly records this as an "unregistered collective investment scheme under the Financial Services and Markets Act 2010"

.jpg)

Comments

Post a Comment