The trade effect of negative interest rates

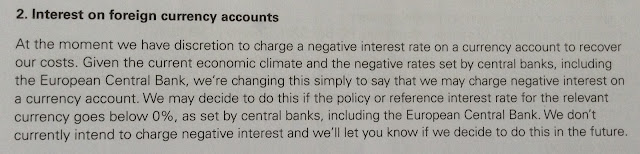

Yesterday, HSBC prepared the ground for imposing negative rates on business depositors. This is an excerpt from HSBC's letter announcing the necessary change to the Terms & Conditions of HSBC business accounts:

Now, this requires some explanation. Firstly, the change applies only to BUSINESS accounts. Retail depositors are unaffected. Secondly, it applies only to currency accounts, not sterling accounts. And thirdly, despite HSBC's mention of "negative rates set by central banks including the European Central Bank", the relevant "policy or reference rate" at present is still positive everywhere except Sweden, where the policy rate is currently -0.35%.

Central banks set several interest rates, of which only one is the so-called "policy rate". The policy rate is usually the rate at which the central bank will lend to banks against good collateral: it is the benchmark not only for the interbank lending rates (Libor, Euribor and their relatives), but also for retail and wholesale bank lending rates: for example, in the UK, standard variable mortgage rates (SVRs) are typically priced as base rate plus margin.

For the US, the "policy rate" is the Fed Funds Rate. For the UK, it is "bank rate" or "base rate". And for the ECB, it is the "main refinancing operations" (MRO) rate. The rate that HSBC refers to in its letter is the MRO rate. In effect, it is saying that if the MRO rate falls below zero, it may impose a negative rate on Euro deposit accounts held by UK business customers.

The MRO rate falling below zero is not as unlikely as it sounds. Currently, the Fed Funds target rate is 0.5%, as is the Bank of England's base rate: the Fed raised rates in December 2015, and the Bank of England has just decided to leave the base rate on hold. But the ECB has been progressively cutting interest rates since 2011. As this chart from the ECB shows, the ECB's deposit rate has been negative since June 2014 (this is the "negative rate" that people talk about), though it was recently reduced further. But more importantly, the MRO rate is only just above zero, at 0.05%:

The ECB is widely expected to cut interest rates further because of continued poor economic performance and very low inflation in the Eurozone. Dropping the MRO rate below zero is no doubt one of the options being considered.

So what is the impact on banks of a negative refinancing rate? Clearly, since policy rates are benchmarks for bank lending rates, it forces down the price of new lending. Currently, banks like HSBC have resisted the temptation to cut deposit rates below zero in response to the ECB's negative deposit rate, because they have been able to maintain their net interest margins by keeping lending rates up. But downwards pressure on benchmark lending rates would squeeze their margins. So HSBC is giving notice that if the ECB pushes the MRO rate below zero, the cost to them of reducing the price of new lending in Euros may be passed on to businesses in the form of a negative interest rate on Euro deposits.

But hang on. HSBC is a British bank, and the letter has been sent to UK business customers, most of whom have sterling accounts. And these days, foreign currency payments can be made directly to sterling accounts with the bank managing the currency exchange. So who would this affect?

It would affect any business which is doing sufficient business with the Eurozone to justify having a Euro account. Particularly, businesses which are both exporting to and importing from the Eurozone, perhaps importing raw materials and parts and exporting finished goods. A negative MRO rate would, in effect, be a tax on UK businesses doing business with the Eurozone.

Now it could be argued that if a UK business faces the equivalent of a withholding tax on sales to the Eurozone, this would benefit Eurozone businesses. But if HSBC can apply this tax to its UK clients, so too can Eurozone banks to their Eurozone customers. So I wouldn't bet on this effect, personally.

It does, however, seem possible that businesses - both Eurozone and foreign - might push the cost on to customers by raising the price of goods and services. This would help bring Eurozone inflation back towards its target. But raising inflation by deliberately increasing business costs is contractionary: it would do absolutely nothing for the Eurozone's chronic demand deficiency. And businesses might choose to absorb the cost by putting downwards pressure on wages and - if possible - supplier prices, by cutting investment and even by laying off staff. They might also reduce dividends to shareholders. Given this, is hard to see how a negative MRO rate would constitute "expansionary policy".

I've argued before that negative rates are not expansionary. At that time, I hadn't thought about the trade effects. But looking at the trade effects now just confirms my view. Negative policy rates would make the Eurozone's economic performance worse. Don't go there.

Related reading:

https://market-ticker.org/akcs-www?post=231071

ReplyDeleteKarl Denningers take on a negative world.

Its my opinion they are forcing consumption chiefly through the American and euro car bubble.

Wealth is being destroyed yet they want MORE.

How long can the credit monopoly maintain concentration ?

Until we have no more to subtract .

Typical MMT guy .

ReplyDelete"Why we need bubbles "

In the natural world nothing runs at full capacity for very long.

"Savings " accumulated = waste.

Savings are necessary but it should never be the goal.

Just as a infinite autumn harvest is a absurdity.

( The crop would spoil)

It is no coincidence that Irish deposits are rising as more and more waste machines get on the roads in almost Celtic tiger quantity .

People are given no choice but to save or not spend.

The car / credit machine does the spending independent of your actions.

In fact it uses your frugality to increase waste production elsewhere.

A truly demonic and anti human system.

This guy should publish more and more stuff .

ReplyDeleteWe can thus save more and more of his files for future enjoyment .

He gives MMTers a bad name which can only be a good thing .

http://monetaryrealism.com/we-need-bubbles/

Dork, please set up your own blog and stop using mine to grandstand your ideas. You are WAY off topic, once again.

ReplyDelete

ReplyDeleteif lending rates fall , volume will rise .

profits may increase .

if mro represents some kind of funding cost ,

margins for new loans will not be affected .

banks may have avoided deposit charge by lending out reserves .

but with - ve mro ,

now nowhere to hide .

Jerred,

DeleteYou've ignored the negative deposit rate, which is a tax on bank holdings of excess reserves at the central bank. Banks holding excess reserves do not fund themselves in the interbank market, since they have no reason to do so. Cutting the MRO therefore makes no difference to funding costs, but it DOES influence benchmark rates. Therefore negative MRO would squeeze margins.

If you think I am wrong, perhaps you would like to advance your own explanation for HSBC's advance warning of negative rates to business depositors in the event of a negative MRO? I assure you the letter is not a fake.

mro falls , and real economy variable loan rates fall . so how does mro fall ? after q e , is c b collateralized lending significant ? interbank loan rates go - ve , if deposit rates go further negative . do r e v l go negative ? redistribution >>> creditors to debtors ?

DeleteFrancis

ReplyDelete20th century inflation is over

Indeed 16th century inflation dynamics is over.

It has always been catastrophic for humanity .

We are witnessing its end.

However the controllers will end most of our lives before the coming dark ages .

Its the only logical thing to do if you want to remain on top of the capitalist dung heap.

Sadly in the final analysis you are a apologist for British credit banking ,( see pure evil.)

I do not understand why almost all economic commentators take such a position.

It must be a LSE mind trick .

That's it , I am signing off.

I hope you and Brian credit bubble Lucey will continue to sing each others praises.

He is such a wonderful British Irishman.

A model (drone ) subject of the Castle.

Car loans and the like increase both physical waste and deposits.

ReplyDeletePeople and companies subsequently hoard their deposits because if they spent them in the current waste based economic ecosystem they would starve , face bankruptcy or at the very least lose their nominal independence.

It is logical individually to board deposits but is also illustrative of the sickness within the system (the economy is currently not designed around human production / consumption)

The CB solution is to seize people accounts , to seize their freedom.

Rather then tackling the waste based practices of their little sisters directly .

In other words to maintain the monopoly of credit at all costs

It obvious to me now this is a deeply religious war against humanity as nobody could accidentally fuck up a system to the degree witnessed.

Its simply impossible.

"Clearly, since policy rates are benchmarks for bank lending rates, it forces down the price of new lending. "

ReplyDeleteMRO isn't a "benchmark" it's a floor, but loans might track the rate. But I see absolutely no reason banks have to reduce lending rates just because MRO falls - the only explanation is if you believe lending is perfectly competitive - but even under perfect competition banks won't reduce lending rates so low until they make negative margins.

" But downwards pressure on benchmark lending rates would squeeze their margins. "

Why? You need to explain this, not just assert it.

Also you should probably mute Dork, he's a lunatic.

ReplyDeleteYep , I hear voices see.

DeleteThis is a far more effective solution.

https://m.youtube.com/watch?v=1U1PM-p3860

How would a negative refinancing rate even work, wouldn't every bank just maximally borrow from the ECB at negative rates for risk free profit, it doesn't make sense. I doubt any central bank will go negative with refinancing rates.

ReplyDeleteUsing this argument, would not any reduction in interest rates be contractionary? With 5% interest rates, business are earning extra revenues thanks to their bank deposits. Cut interest rates to 3%, they are earning less revenues. To maintain margins, they might raise prices or cut wages, which you say is contractionary. Turning the argument around, riaisng interest rates is expansionary. I think there is something missing here.

ReplyDeleteIf there's no change to lending, this would hold true. Interest paid by the central bank is added to the money supply. Reducing it would thus be contractionary. But normally credit expands when rates are lowered, and vice versa, which dwarfs the reduction of interest paid to the private sector.

Delete

ReplyDeleteSteve from Virgina in one of his better moments .

"Credit money expansion (Banks) replaces a great debt with another, greater debt. There is never a net reduction in the debt, only a perpetual increase.

(we are reducing our debt by exporting our debt / symbolic wealth via goods export elsewhere destroying internal commerce)

Treasury money expansion is repudiation of debts => repudiation of (pre-existing) money, institutionalized default (expansion includes purposeful inflation).

Finance offers fiat debt then demands repayment in circulating currency (gold clause effect). Fiat currency offered by the government to retire fiat debt: both the debt and the currency are extinguished at once.

The creditor says, “You owe us, you must pay with circulating money!”

The debtor says, “There is no circulating money, the creditors refuse to lend …”

The creditor says, “We will seize your property instead and destroy your economy!”

The government (which is also a debtor) says:

– “We will create money without borrowing and repay the loans as they come due. We can do this because we are the government, our money is paid to our army.”

– “The loans are fiat — they were created by the lender with the stroke on a keyboard, they were not made from circulating currency. To act as if they were is a crime, a false claim. The lenders will be repaid by a stroke of the keyboard, in the same form as the debts were issued. If you or other lenders touch our property or our citizens we will throw you into prison and decide later whether to feed you or not.”

– “Because lenders have impoverished our country with endless false claims we will punish you severely whenever we can get our hands on you. You are our enemy and we will destroy you if we can, because you have sought to destroy us!”

Instead of this reality debated in Ireland we have the surreal "fiscal space" argument .

ReplyDeleteGerry Adams of Sinn Fein was asked about this fiscal space thingy yesterday.

Cue classic Irish King Goshamk politics .

Instead of explaining this is the drop of blood given back after the pound of flesh is extracted he deferred meekly to his "finance expert "

I look forward to Sinn Fein getting hold of "power"

They can finally be exposed as capitalist undertakers.

Finally the Irish people might wake the F£$k up just as the Greeks must have done in 2015.

As far as I am aware Irish M2 has been static or falling for 2 years longer then the 30s depression and trade war.

ReplyDeletePerhaps good Brian can provide the 1930s charts for confirmation.

A recent rise of overnight deposits has been witnessed .

Somewhat larger then the decline of term deposits .

This coincides with 15% ~ growth of 1 to 5 year credit (car loans)

But these car / corporations will want their money back ( the currency will not remain in circulation even at 0% interest)

What happens then ?

More human contraction / car expansion.

http://psalmistice.com/2015/06/18/on-principal-and-interest-hermetic-magick-and-the-lords-of-time/

ReplyDeleteThe time value of money is the most successful deception ever attempted.

But negative rates is also usury , it is a mere inversion of present practices.

The goal remains the same.

Concentration of wealth .

At this present time, so-called “ZIRP” (Zero Interest Rate Policy) and even “NIRP” (Negative Interest Rate Policy) is spreading all over the moribund economies of the Western world. We now receive zero interest on money deposited in a savings account. Not only that, in an increasing number of Western countries, the Lords of Time are now charging interest (ie, paying negative interest) on money deposited in a savings account. Yes, that’s right … if not now, then very soon, they will charge you interest for “holding” money on deposit in the “safe-keeping” of their bank.

ReplyDeleteWhy are they doing this? As with so many magician’s tricks, the key to successfully pulling off the illusion, is movement. In the sideshow hustler’s game of Thimblerig or Three Shells and a Pea28, the faster the hustler moves his hands, the more difficult it is to see that he has moved or even pocketed the pea.

In the great alchemical trick of Hermes the Thrice-Greatest and his Latter-Day Saints, this vital movement is called “Flow”, or the “Velocity of the Circulation of Money”. So long as the flow of money in the economy is fast enough, no one notices that the game is actually rigged. That is, no one notices that there is insufficient money in the system to pay interest.

ReplyDeleteThis policy of zero (or even negative) interest rates on bank deposits, is all about trying to speed up the flow of money in the economy. The Lords of Time are hoping that this policy will encourage people to spend (“Flow”), not save (“Stock-pile”) money.

Why? Because the only way for the Lords of Time to keep on “earning” compound interest on the intergalactic levels of debt that they have lent to the world, is to make the “money” flow fast enough.

The real truth of the Money Illusion is this: If everyone had to settle their debts at the same time, there is always far more money owed, than there is money to pay with. The game only seems to work fairly and honestly if we only look under one shell at any time, and, if we believe the hustler’s claim that the missing pea really is just hiding under one of the other shells all the time

This stops NOW, Dork. You are abusing my hospitality. I've asked you to stick to the topic but you are posting ever weirder stuff. I will delete any more comments you make.

DeleteThis comment has been removed by the author.

DeleteThis comment has been removed by a blog administrator.

ReplyDeleteHi Frances,

ReplyDeletei know this is not directly related, but could you comment more on why Policy Rates influence the rest of rates. I understand that MRO is an auction of money at a specific price. How is the auction conducted and how is the price set? I've been searching for clearer explanations, but I stumble with some of the jargon.

Thanks,

Alex

If buisinesses are going to be spending time and effort in applying deposits to unprofitable activities in order to avoid making a loss on deposits then that is a distraction from actual productivity.

ReplyDelete"But what is inflation? The usual response is "an increase in money supply." Uh, not really.

ReplyDeleteRemember the basic economic equation: MV = PQ

That is, Money (and credit) * Velocity (how many times each "turns over" in a given unit of time) = Price (of each thing or service produced) * Quantity (how many things or services are produced)

This is an equation, which means it always balances. It must, by definition.

So what does a negative rate do? It decreases "M". That is, if you deposit funds over time you have fewer of them.

But wait -- the goal is to increase M*V -- that's "inflation."

So why do it?

Because you are trying to force up "V" -- velocity. That is, you're trying to force those with money to put it into the economy, and keep it there; that is, remove it from said deposits (or the mattress) and spend it.

But why would you do that? You'd only do that if you believed spending it would benefit you -- either as an investment (that is, you can spend some money in the expectation of producing even more as a consequence) or out of pure consumption.

But you will only invest if you believe the future is bright; that is, that your investment will pay off.

What does a central bank that invokes desperate measures such as this tell the market?

It tells the market the future sucks and so we're going to try to force you to behave as we wish."

Karl Deninnger - The Market Ticker Jan 31 2016

So the policy response is to subtract your deposit over time (Demurrage) and at the same time issue the most wasteful credit imaginable (consumer credit for cars)

Demurrage on its own might be fair means of managing society but its use in conjunction with bank credit is devastating

UK trade figures published for 2015.

ReplyDeleteAs I have suspected , goods deficit increased to £125 Billion despite the drop in oil prices.

This is primarily because the deficit with the EU28 increased from 79 billion to 89 billion with poor countries such as Spain pushed into ever increasing goods surplus.

This trade dynamic is not one of comparative advantage.

Its the more traditional usurer vs victim model.

The FT this morning stated this was just terrible..... when in fact it was the objective from the start.

They claim more efforts must be vectored toward UK exports ( cue behind door laughter)

When the core problem is lack of national and sub national production / consumption in both the deficit and surplus country.

Was the EU designed to prove (the partially correct) dependency theory ?

ReplyDeleteLooks like it......

Hi Frances,

ReplyDeleteI’d like to restate your point combining the content of your 2 posts about NIRP to be sure it’s clear to me.

In my understanding the essential problem is that NIRP is destroying one of the fundamental mechanisms Commercial Banks use to finance themselves: arbitraging the difference between a Commercial Bank Deposit and a CB (Central Bank) Deposit. I guess this is what you call “the margin squeeze”

So basically CBs are introducing a new (artificial) cost in the system and Commercial Banks have to decide how to deal with it.

Unfortunately for CBs (and for the people) Commercial Banks have not just one option (the one CB wants hence increase lendings) but more than one.

Commercial Banks could

- reduce excess reserves buying Sov Debt of AAA countries (it’s already happening)

- pass the new cost into the system, distributing it among lenders (reducing savings remuneration or increasing its cost) and borrowers (increasing bank lending costs)

As you have correctly observed, the latter strategy could probably make deflation even worse as in a context of low demand, the excess cost would probably be absorbed by cost cuttings.

Moreover lending is a two-actors complicated process: the two actors (lender and borrower) need to be both willing to conclude the deal but perceived risk by both sides is so high that this is very unlikely to happen.

Basically I think the main reasons for this risk perception so high are the following ones

- there is no mature Economy which is driving the global one (the long wave of EZ and US demand collapse started some years has finally hit the emerging countries and China and Japan as well)

- the big finance deregulation pulse started in the ‘80ies has produced a very unstable system (similarly as it was in the past, i.e. ‘20eis)

- the Ruling Class (Central Bankers and Politicians) is managing the present (complicated) situation with non-standard solutions hence leading everyone in the unexplored territories of NIRP, high unemployment, …

- the “transient” dynamic of a pervasive processes like globalization finished and considering the reached equilibrium point does not seem very satisfactory a new pulse will probably be needed

- finally the Production System designed around the idea of “middle class” (hence consisting of high volumes of very standardized products) has collapsed as the above mentioned phenomena are finally destroying the “middle class” itself hence the ultimate source of demand … so a new Production System needs to be designed

What do you think about it ?

Tnx

nice post.

ReplyDeleteHi, Is there anyone out here who can teach me about forex trading.

ReplyDelete