OSI, PSI, the IMF and fantasy

After much intense negotiation, it seems there is a new deal for Greece. Or at least that is how it has been presented in the media. But what sort of deal is it, and does it solve the Greek problem?

The wording of the Eurogroup's statement does not suggest that there is a "deal", as such. All it says is that the official sector - the ECB and Eurogroup - may be prepared to accept poorer returns on their holdings of Greek debt. The specific measures that they "would consider" are the following:

None of these measures is "officially" a writedown of Greek debt. The face value of the debt will remain the same, which will enable politicians in creditor countries such as Germany to claim that Greece is not being "forgiven" its debt. But this is misleading. The value of debt is given not just by its face value, but by the return that it generates. Cutting the interest rate (and, in the case of the Eurosystem, refunding interest paid) reduces the return on debt. This is because over time, money loses value due to inflation, so the face value of a 10-year bond is less in "real terms" at maturity than it is at issue: the interest on the bond compensates for this loss in value, plus the opportunity cost to the lender of not having that money available for other things. Cutting the interest rate reduces the compensation to the lender, and if the interest rate falls below the inflation rate during the lifetime of the bond, the lender actually loses money as the value of the principal is eroded. Extending the maturity of debt also effectively reduces the return to the lender, since that money is "tied up" for longer, increasing the risk of principal loss. Therefore these measures constitute a writedown of the value of Greek debt held by the official sector, in much the same way that Brady Bonds reduced the value of Latin American debt in the 1980s.

For Greece, the effect is a reduction in the anticipated debt burden by 2020. Now this is something of a moving target. Sovereign debt is usually quoted as a percentage of GDP, and this is how the Greek debt burden is presented. So it is not just the actual amount of debt in euros that matters, but the performance of the Greek economy.

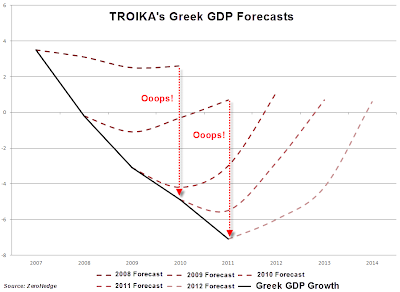

Each time a bailout deal has been agreed for Greece, estimates of its expected GDP over the next 10 years have been produced. But every estimate has been wrong - and not just slightly wrong, but totally wrong in both the scale and the direction of GDP growth. As this graph from Zero Hedge shows, every estimate has assumed a return to strong positive growth and creation of a primary budget surplus within a year or two of the deal:

But the reality is that the Greek economy has been falling down a recessionary black hole: with each year that passes, economic activity declines, tax revenues fall and the prospects for return to positive growth, let alone a primary budget surplus, recede futher into the distance. The swingeing cuts Greece has made to its budget to meet Troika demands have singularly failed to make any significant dent in its deficit: all they have done is trash its economy. And the debt pile grows ever larger, both in reality as Greece is forced to borrow more money to meet its essential spending commitments and service its debt, and as a percentage of GDP, as GDP falls ever lower.

The estimates on which this deal depends are that Greece returns to strong growth by 2015 and runs a primary budget surplus (i.e. after debt service) of at least 4.5% from 2016 onwards. If they manage to achieve this AND both the debt buyback and the official sector NPV haircut go ahead, their debt will be at 124% of GDP in 2020, which is supposedly sustainable - although many people would doubt that this is sustainable in practice. Without those measures, the debt level would be 144% of GDP, which is almost certainly unsustainable, and if Greece fails to achieve the growth and budget targets then the level will be even higher - some estimates have put it as high as 190% of GDP.

The significance of keeping debt at "sustainable" levels is that the IMF, which is a contributor to the bailout funds agreed in March 2012, cannot lend to countries with unsustainable debt. Therefore the bailout ALREADY AGREED depends on reduction of the debt burden to a "sustainable" level. You may ask how on earth the bailout was agreed in the first place if the debt wasn't sustainable. But remember what I said about GDP estimates far exceeding reality? The debt itself hasn't risen much more than expected. But GDP is far lower. Therefore a debt that in March was expected to be "sustainable", has turned out to be anything but.

So are the latest estimates of GDP any more reliable than the previous ones? I seriously doubt it. The Greek economy is now in its sixth year of deep recession and shows no signs of recovery. I suspect that Greece's GDP is falling back to where it was when Greece joined the Euro, since the whole of its economic growth during its Euro membership has been generated by debt-fuelled consumption rather than increased production of real goods and services. In fact since the Greek economy has actually lost competitiveness compared to its neighbours, its GDP may have to fall even further. In which case this chart shows that it still has an awfully long way to go:

Note: the flattening of the GDP line in 2010-11 does not indicate that GDP is static, it means that the World Bank does not have up-to-date figures. The ZeroHedge chart above shows that GDP has been on a steeply downward trend since 2008.

If I am right, there is little chance of recovery any time soon. And this also makes the target of a 4.5% primary surplus from 2016 highly unlikely. But even if Greece by some miracle managed to achieve this, the terms of the bailout are that all of that surplus plus 30% of any excess must go towards debt reduction, rather than being invested in the Greek economy. It is very, very hard to see how the Greek economy can possibly return to strong growth if all its deficit reduction efforts simply enrich its creditors. Sadly, I think it is far more likely that Greek GDP will continue to shrink, achieving primary surplus will drift further and further out of reach and the debt pile will grow ever larger. And both official and private sector creditors will eventually have to accept that Greek debt simply is not repayable. Further writedowns will inevitably follow. Not that there will be much scope for further reduction of private sector holdings; the private sector took losses of around 75% of NPV on its bond holdings earlier this year, when the Greek government coercively swapped "new bonds for old". And the debt buyback in the current deal is redemption of those new bonds at 28% of face value. That really doesn't leave much Greek debt in the private sector. The media headlines have focused on the official sector's contribution this time: but the private sector is being asked to take a much larger hit.

Not surprisingly, the private sector is fighting back. The Greek banking lobby has protested that the buyback at 28% would bankrupt them (link h/t @Alea_), and called for additional EFSF funding to restore their capital levels if they sell their holdings - which they feel psychologically bound to do, even though it seems unlikely that the government could impose a second coercive debt restructuring on the private sector.

This sounds odd to me. The redemption price is the average market price of those bonds at close of business on 23rd November. The bonds should already have been marked to market if they are held for trading purposes, so the banks should already have taken the hit on their profit & loss accounts. If they haven't, then either the bonds were intended to be held to maturity or they have not been marked to market properly. If the former, then redemption at such a discount would indeed cause serious losses - although it could be argued that holding distressed government debt at par, even to maturity, is perhaps not the wisest investment strategy. But I suspect the latter. The market price for Greek bonds has indeed fallen by 70% since the new issue, but the market has been thin for quite some time, which tends to make market prices volatile. Holders of Greek bonds are therefore likely to have marked them to some kind of model, no doubt using parameters that flatter the value of the holding. This is similar to the methods used for valuing CDOs in the run-up to the financial crisis, and the outcome might well be similar too.

So the debt buyback could cause widespread bankruptcy of Greek financial institutions. This seems utterly counter-productive, given that the bailout funds were partly intended to recapitalise the Greek banking system. I don't have a great deal of sympathy for financial institutions that take a grossly unrealistic view of the value of their bond holdings, but collapse of the Greek banking system as a consequence of the debt buyback would be ludicrous.

It is also by no means clear where Greece will find the money for this buyback. Ollie Rehn insists that Greece will have "all the money it needs" for the buyback, but there is no new money on the table, the 2nd bailout funds have not yet been disbursed and the "additional measures" - including the refund of Eurosystem interest payments, which seems the most obvious source of funds - are conditional on successful completion of the buyback. Maybe I'm missing something, but I can't see how this buyback can succeed with nothing but imaginary money.

In fact the whole deal looks like fantasy. A debt buyback funded from thin air and possibly resulting in bankruptcy of a newly-recapitalised banking system: yet more wishful thinking on GDP figures: official sector involvement that is dependent on meeting impossible conditions. And above all, no recognition of the reality of the Greek situation. Greece's debt is unpayable and and its economy is falling off a cliff. It needs comprehensive debt forgiveness and the equivalent of a Marshall plan to restore its economy to health, not fiscal "reforms" that drive it further into the ground with large amounts of Eurofudge to keep its official creditors sweet while stiffing the private sector.

The IMF is evidently uncomfortable with the hard line taken by the Eurogroup and the ECB, and this is the closest it has ever come to pulling the plug on the whole deal. I really wish it had done so. This Greek tragedy must be brought to an end before it becomes a global disaster.

The wording of the Eurogroup's statement does not suggest that there is a "deal", as such. All it says is that the official sector - the ECB and Eurogroup - may be prepared to accept poorer returns on their holdings of Greek debt. The specific measures that they "would consider" are the following:

- 1% reduction in interest rates on the loans made available under the "Greek Loan Facility" (the first bailout)

- 0.1% reduction in the fees paid by Greece for EFSF guarantees of its debt

- deferral of interest for ten years on EFSF loans (the second bailout)

- extension of maturities on EFSF and bilateral loans by fifteen years

- repatriation of interest paid by Greece to the ECB and national central banks (the "Eurosystem")

None of these measures is "officially" a writedown of Greek debt. The face value of the debt will remain the same, which will enable politicians in creditor countries such as Germany to claim that Greece is not being "forgiven" its debt. But this is misleading. The value of debt is given not just by its face value, but by the return that it generates. Cutting the interest rate (and, in the case of the Eurosystem, refunding interest paid) reduces the return on debt. This is because over time, money loses value due to inflation, so the face value of a 10-year bond is less in "real terms" at maturity than it is at issue: the interest on the bond compensates for this loss in value, plus the opportunity cost to the lender of not having that money available for other things. Cutting the interest rate reduces the compensation to the lender, and if the interest rate falls below the inflation rate during the lifetime of the bond, the lender actually loses money as the value of the principal is eroded. Extending the maturity of debt also effectively reduces the return to the lender, since that money is "tied up" for longer, increasing the risk of principal loss. Therefore these measures constitute a writedown of the value of Greek debt held by the official sector, in much the same way that Brady Bonds reduced the value of Latin American debt in the 1980s.

For Greece, the effect is a reduction in the anticipated debt burden by 2020. Now this is something of a moving target. Sovereign debt is usually quoted as a percentage of GDP, and this is how the Greek debt burden is presented. So it is not just the actual amount of debt in euros that matters, but the performance of the Greek economy.

Each time a bailout deal has been agreed for Greece, estimates of its expected GDP over the next 10 years have been produced. But every estimate has been wrong - and not just slightly wrong, but totally wrong in both the scale and the direction of GDP growth. As this graph from Zero Hedge shows, every estimate has assumed a return to strong positive growth and creation of a primary budget surplus within a year or two of the deal:

But the reality is that the Greek economy has been falling down a recessionary black hole: with each year that passes, economic activity declines, tax revenues fall and the prospects for return to positive growth, let alone a primary budget surplus, recede futher into the distance. The swingeing cuts Greece has made to its budget to meet Troika demands have singularly failed to make any significant dent in its deficit: all they have done is trash its economy. And the debt pile grows ever larger, both in reality as Greece is forced to borrow more money to meet its essential spending commitments and service its debt, and as a percentage of GDP, as GDP falls ever lower.

The estimates on which this deal depends are that Greece returns to strong growth by 2015 and runs a primary budget surplus (i.e. after debt service) of at least 4.5% from 2016 onwards. If they manage to achieve this AND both the debt buyback and the official sector NPV haircut go ahead, their debt will be at 124% of GDP in 2020, which is supposedly sustainable - although many people would doubt that this is sustainable in practice. Without those measures, the debt level would be 144% of GDP, which is almost certainly unsustainable, and if Greece fails to achieve the growth and budget targets then the level will be even higher - some estimates have put it as high as 190% of GDP.

The significance of keeping debt at "sustainable" levels is that the IMF, which is a contributor to the bailout funds agreed in March 2012, cannot lend to countries with unsustainable debt. Therefore the bailout ALREADY AGREED depends on reduction of the debt burden to a "sustainable" level. You may ask how on earth the bailout was agreed in the first place if the debt wasn't sustainable. But remember what I said about GDP estimates far exceeding reality? The debt itself hasn't risen much more than expected. But GDP is far lower. Therefore a debt that in March was expected to be "sustainable", has turned out to be anything but.

So are the latest estimates of GDP any more reliable than the previous ones? I seriously doubt it. The Greek economy is now in its sixth year of deep recession and shows no signs of recovery. I suspect that Greece's GDP is falling back to where it was when Greece joined the Euro, since the whole of its economic growth during its Euro membership has been generated by debt-fuelled consumption rather than increased production of real goods and services. In fact since the Greek economy has actually lost competitiveness compared to its neighbours, its GDP may have to fall even further. In which case this chart shows that it still has an awfully long way to go:

Note: the flattening of the GDP line in 2010-11 does not indicate that GDP is static, it means that the World Bank does not have up-to-date figures. The ZeroHedge chart above shows that GDP has been on a steeply downward trend since 2008.

If I am right, there is little chance of recovery any time soon. And this also makes the target of a 4.5% primary surplus from 2016 highly unlikely. But even if Greece by some miracle managed to achieve this, the terms of the bailout are that all of that surplus plus 30% of any excess must go towards debt reduction, rather than being invested in the Greek economy. It is very, very hard to see how the Greek economy can possibly return to strong growth if all its deficit reduction efforts simply enrich its creditors. Sadly, I think it is far more likely that Greek GDP will continue to shrink, achieving primary surplus will drift further and further out of reach and the debt pile will grow ever larger. And both official and private sector creditors will eventually have to accept that Greek debt simply is not repayable. Further writedowns will inevitably follow. Not that there will be much scope for further reduction of private sector holdings; the private sector took losses of around 75% of NPV on its bond holdings earlier this year, when the Greek government coercively swapped "new bonds for old". And the debt buyback in the current deal is redemption of those new bonds at 28% of face value. That really doesn't leave much Greek debt in the private sector. The media headlines have focused on the official sector's contribution this time: but the private sector is being asked to take a much larger hit.

Not surprisingly, the private sector is fighting back. The Greek banking lobby has protested that the buyback at 28% would bankrupt them (link h/t @Alea_), and called for additional EFSF funding to restore their capital levels if they sell their holdings - which they feel psychologically bound to do, even though it seems unlikely that the government could impose a second coercive debt restructuring on the private sector.

This sounds odd to me. The redemption price is the average market price of those bonds at close of business on 23rd November. The bonds should already have been marked to market if they are held for trading purposes, so the banks should already have taken the hit on their profit & loss accounts. If they haven't, then either the bonds were intended to be held to maturity or they have not been marked to market properly. If the former, then redemption at such a discount would indeed cause serious losses - although it could be argued that holding distressed government debt at par, even to maturity, is perhaps not the wisest investment strategy. But I suspect the latter. The market price for Greek bonds has indeed fallen by 70% since the new issue, but the market has been thin for quite some time, which tends to make market prices volatile. Holders of Greek bonds are therefore likely to have marked them to some kind of model, no doubt using parameters that flatter the value of the holding. This is similar to the methods used for valuing CDOs in the run-up to the financial crisis, and the outcome might well be similar too.

So the debt buyback could cause widespread bankruptcy of Greek financial institutions. This seems utterly counter-productive, given that the bailout funds were partly intended to recapitalise the Greek banking system. I don't have a great deal of sympathy for financial institutions that take a grossly unrealistic view of the value of their bond holdings, but collapse of the Greek banking system as a consequence of the debt buyback would be ludicrous.

It is also by no means clear where Greece will find the money for this buyback. Ollie Rehn insists that Greece will have "all the money it needs" for the buyback, but there is no new money on the table, the 2nd bailout funds have not yet been disbursed and the "additional measures" - including the refund of Eurosystem interest payments, which seems the most obvious source of funds - are conditional on successful completion of the buyback. Maybe I'm missing something, but I can't see how this buyback can succeed with nothing but imaginary money.

In fact the whole deal looks like fantasy. A debt buyback funded from thin air and possibly resulting in bankruptcy of a newly-recapitalised banking system: yet more wishful thinking on GDP figures: official sector involvement that is dependent on meeting impossible conditions. And above all, no recognition of the reality of the Greek situation. Greece's debt is unpayable and and its economy is falling off a cliff. It needs comprehensive debt forgiveness and the equivalent of a Marshall plan to restore its economy to health, not fiscal "reforms" that drive it further into the ground with large amounts of Eurofudge to keep its official creditors sweet while stiffing the private sector.

The IMF is evidently uncomfortable with the hard line taken by the Eurogroup and the ECB, and this is the closest it has ever come to pulling the plug on the whole deal. I really wish it had done so. This Greek tragedy must be brought to an end before it becomes a global disaster.

Dividing as you do between "official" and "private" creditors we must remember that austerity twirls around the "public" and not the more proper market, and in doing so be sure to not forget that if one actually cares to seriously analyse the "public" cuts to expenditure that Greece has undertaken over the past few years, nothing of much significance has occurred. Greek politicians and their friends continue to enrich themselves through a Byzantine complex of procedural obscurity while the people they ostensibly "serve" continue to commit suicide in ever greater numbers.

ReplyDeleteIn public discourse, a double-dip recession is widely regarded as a greater concern than default or the collapse of the euro area...but austerity is preferable to default both for the nation in question and its creditors...Austerity should be like removing a bandaid, with "public" spending not slowly peeled back over months and years, but cut by 75% overnight. A wake up obliging people to reorganise how they work on a daily basis. Education systems will adapt. So too will health care. This time is different

ReplyDeletehttp://www.piie.com/publications/pb/pb12-22.pdf

How you can claim that completely removing the safety net overnight for the poorer and weaker members of society is preferable to creditors taking losses beggars belief, frankly. Where is your compassion?

DeleteThis time is only different because the Eurozone countries have prematurely adopted a single currency which seriously restricts their ability to control their economies and forces them to inflict suffering on their population. It's like a Gold Standard with knobs on, and it is causing the same problems as the Gold Standard did in the early years of the Depression.

I agree there would be serious risks involved in its breakup and I am not suggesting that. I AM suggesting that the cowardly behaviour of the official sector in yet again avoiding the real issues will only make a bad situation worse. Greek debt is unpayable: the GDP estimates are fantasy: substantial official sector debt writedown, without impossible economic performance conditions, is now the only viable course of action and the sooner it is done the better. Unfortunately this won't happen because politicians in ALL countries will look after themselves rather than do the right thing. This deal kicks the can down the road yet again because the right deal would have trashed Merkel's chances in the German elections.

The welfare state institutionalises poverty through alleviating pressure for good governance by substituting force for philanthropy, establishing a deceitful body of self-interested politicians between givers and receivers. In the digital age, philanthropy is Itunes, say, with welfare being the bankrupt HMV.

ReplyDeleteThere's a beautiful song by a wonderful African American Artist titled

ReplyDeleteMr/Ms Intentional: highly recommended. Wonderful voice and lyrics highly relevant to our discussion! :-)

https://www.youtube.com/watch?v=a8BgPaLZtWg

I must say I like your saying that the official sector is not playing up to what we reasonably can expect of them, but ask you if submitted to similar forms of regulatory disciple (namely, Law based on the sanctity of private property & thus contractual obligations) for the sake of more direct accountability vis a vis the particular, "official" individual creditors, would not the "official creditors" be more likely to act co-operatively compared to now, this situation in which there is literally no force except that emanating from wise individuals of the public like yourself in the form of social pressure, which restricts their apparently maniacal modus operandi? The rule of law can't be that bad of a thing!

ReplyDeleteBear in mind one man from this "official creditor" has left for all to see on the public record his comment that when things get a bit tricky "we have to lie!" Now just imagine if the CEO of BP or Gazprom or any other company you can imagine, actually said to the FT, for example..."look, sometimes, if the incoming figures aren't looking that good, we have work around such issues with KPMG to maintain confidence in the market place"... !? Look at Muddy Waters and this crazy Ponzi run out Singapore: this is real-time and actually effective regulation occurring, driven by a for profit short seller sniffing out fraud through a dedicated team of people able to devote the time needed in as expert a manner as obviously required to sift through complex issues to help reduce false claims in this market which wrongly invite people to waster otherwise good capital. This is regulation, alright, only it's actually working for once.

ReplyDeleteIn a way, most religions place a heavy emphasis on honesty, or at least a vague definition of virtue which tends to include ideas like or associated with honesty, and I have to say I think honest generally performs a far greater service to society than does dishonest, and I suspect you would agree. Well, why is that? That's such a complicated question! I've said enough already, us usual, but the idea that short sellers as regulators in a new information economy driven by digital currencies whose alleged integrity is upheld by trust, in not only the particular currency but also the surrounding eco system of local (or global) businesses is kinda cool...This TED talk discusses that. How to price trust? Let's see who we can trust! A price might help :)

ReplyDeletehttp://www.ted.com/talks/rachel_botsman_the_currency_of_the_new_economy_is_trust.html

Markets are naturally biased towards clear commentary that seems honest, profit lies therein.

ReplyDeletehttp://www.zerohedge.com/news/2012-11-30/guest-post-myth-austerity

"Sovereign immunity" (just like "diplomatic immunity") produces extreme forms of inequality before the eyes of the Law: a two-tiered system of arbitration depending on how connected you are. What is democratic about that? Of course, it is the exact opposite to any fair definition one would want to attribute to a "fair and democratic society".

ReplyDeleteThe multi-billion-dollar fight for national sovereignty

http://www.reuters.com/video/2012/11/30/reuters-tv-the-multi-billion-dollar-fight-for-natio?videoId=239548847&videoChannel=117757

But, to any smart body who's intellectually honest in their thinking, that should not come as a surprise

http://economics.org.au/2011/08/government-is-in-a-state-of-anarchy/

Almost every comment on this post seems to have nothing to do with the subject of the post. Although they are posted anonymously, I strongly suspect all these comments come from the same person, who is effectively using my blog to grandstand his own ideas. Whoever you are, can I suggest you write your own blog, rather than hijacking mine to promote your own agenda? You are welcome to post here, but I would appreciate it if you would please confine yourself to discussing the subject of the post.

ReplyDeleteI only wanted a person of your unusual intelligence to see a view dissimilar to your own because competition amongst opposing ideas is what produces higher forms of thought, but your wish is my command. I will adhere to your rules.

ReplyDeleteI do agree with the first part of Anonymous' last comment but to return to your topic, Frances, isn't the issue that, if Greece were the only country in this mess, and the reporting and estimates were done properly, it may be able to recover in the way posited?

ReplyDeleteBut given that almost every other country from which Greece can earn a living - mainly from tourists - is in a similar pickle, it makes it much more difficult for the economy to grow and, as you point out, Greece would effectively be 'fined' for such growth anyway. So what's the point of working for ordinary Greeks?

It seems to me that the whole financial system has dug itself into a hole from which there is no escape unless and until the ECB (in Greece's case) can carry out central bank duties without Germany twisting the ECB's arm. If this eventually comes down to debt forgiveness, then so be it.

There is no example in history of a country recovering from the sort of mess Greece is in purely by means of internal devaluation. Debt deflation never, ever leads to growth - really the Troika could do with reading Irving Fisher. External devaluation is always necessary, nearly always coupled with debt default or forgiveness and often economic aid too.

DeleteThe problem is that the Euro prevents external devaluation, the Troika prevents default, and no way will anyone countenance aid to Greece at the moment. Debt forgiveness is the only possible route, but although this proposal looks like forgiveness, it is so hedged around with impossible conditions that it will never happen. But debt forgiveness, probably with economic aid, is where this tragedy is bound to end.

It is very, very sad that the Greek economy must disintegrate and ordinary Greeks suffer by the thousand for creditors to accept the inevitability of never recovering their money. And it is even sadder that the effects of the abject failure of the Troika to deal with the Greek problem effectively will rebound around the world.

It must ultimately come to pass that the Troika will understand this but the collar that has been put around the Greek people's neck is very painful to watch.

DeleteGreece is being made the sacrificial goat in a possibly vain attempt to stop the contagion passing to the rest of the Euro. Essentially it is small enough not to matter and large enough to serve as a warning.

The only parallel I can think of is Germany post Versailles Treaty. It is possible to claim ignorance then but today with I would have hoped a better understanding of how things work, it does not auger well for political stability in that part of the world.

It is horrible to behold but of course provides a distraction from our own upcoming triple-dip recession because growth is the only answer.

The policy of the Euro elite seems to be neither based on economic theory or human compassion. The euro has become a monster of irrational deflation. As you say a gold standard without the Gold. As for Mr. Anonymous might I suggest he or she have some therapy to correct that streak of sadism he or she suffers from. As Keynes said economics is a moral science; the aim is to increase human happiness not to inflict sadistic punishment on the innocent.

ReplyDeleteKeith, policy per se is sometimes considered with religious zeal nowadays, I presume because it manages to enjoin those who impose it to actually believe that they are vital to the proper functioning of a healthy society. After all, who doesn't appreciate feeling needed?

ReplyDeleteFrances, you said that "debt deflation never leads to growth" but a leading German expert has devoted one entire book to suggesting otherwise - https://mises.org/store/Product2.aspx?ProductId=538. Also, please forgive me for straying off topic, but I know you're quite "modern" insofar as you don't immediately dismiss the idea of "virtual" currencies...well, here also is another interesting point of view that actually seems to postulate that we may in fact need to redefine what now is called "currency" - http://www.ted.com/talks/rachel_botsman_the_currency_of_the_new_economy_is_trust.html

The writer is proposing Mellonist liquidationism, which was shown to have terrible human consequences in the American depression. He can come up with all the theory he wants but the fact is that his ideas have already been tried and found very, very wanting. Sadly the Germans do not seem to have learned from their own liquidationism under Chancellor Bruning, which made their experience of the Depression far worse than it needed to be and led directly to the rise of Hitler.

DeleteI have written elsewhere about virtual currencies. But frankly they are irrelevant as far as the present situation in Europe is concerned.

Whoa, Nelly! Did you read that book, or just repeating pre-determined opinions? What makes you think the US depression underwent a liquidation in the sense that you mean? The history of the depression is far from settled. Different interpretations exist, remember, to claim a monopoly on reality or even history seems a tad presumptuous. According to the hard data in that presentation, virtual currencies are not irrelevant to the real estate market of the capital of Europe's second most important State, France.

ReplyDeleteWhat would happen if central bank employees could not, hypothetically speaking, buy bonds?

Yes, I did read that book, and my interpretation stands. The author is callously unconcerned with the lives of those who would be hurt by such a policy, and is apparently ignorant of hysteresis effects that make recovery from such a deflationary policy unlikely.

DeleteI don't think there is much dissent in the economic community about the contribution of the US's hard-money deflationary policies in the early 1930s to the depth of its depression. Or the same effect in Germany, either.

What happens when central bank employees cannot buy bonds is debt default and a massive economic crash.

Even Krugman, the economic Pope, has stated vis a vis your reference to " Mellonist liquidationism"

ReplyDelete“Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate.” That, according to Herbert Hoover, was the advice he received from Andrew Mellon, the Treasury secretary, as America plunged into depression. To be fair, there’s some question about whether Mellon actually said that; all we have is Hoover’s version, written many years later.

http://www.nytimes.com/2011/04/01/opinion/01krugman.html

It does not matter whether Mellon actually said that. The point is that that was the policy pursued by Hoover, with devastating economic effects.

DeleteBut if you would like to consider the effects of a similar hard-money deflationary approach, look at the policies pursued by Montagu Norman at the Bank of England in the 1920s - and Churchill, of course. Britain did not have much of a depression in the 1930s, but it had had a self-imposed one in the 1920s instead. Ten years of misery due to massive internal devaluation in a misguided attempt to restore the currency to its pre-1914 value. Just like Greece now - it cannot devalue because of the Euro, so it must crush its population's living standards. Utter madness.

Interesting. What are hysteresis effects? And What should have been the response to the economic issues in the 30s?

ReplyDeleteHysteresis is what happens when people are unemployed (or employed in jobs that don't use their skills) for so long that they lose their skills and their motivation and end up unemployable. It's what happens when you have long-lasting depression, or the collapse of a major industry on which a particular area depends (for example mining towns in the UK of the 1980s).

DeleteThe correct response to the economic issues in the 1930s was public spending to replace the private investment that was abruptly withdrawn after the Wall Street Crash, coupled with currency devaluation. It is now firmly established that those countries that tried to remain on the Gold Standard fared far worse in the 1930s than those that abandoned it early. A look at US public and private debt levels in the 1930s shows that for much of the 1930s private debt levels were falling sharply, but public debt levels ALSO fell - even the New Deal was insufficient, really. The huge increase in public spending in WWII brought the US out of depression. It left high debt afterwards, of course, which was eliminated through a combination of fast growth, financial repression and - later - inflation. I wrote about this here:

http://coppolacomment.blogspot.co.uk/2012/06/dont-do-as-i-say-do-as-i-do.html

Interesting. Do you want a free market in money? It's common logic, of course, that one of the main consumer products that should be completely controlled by practically every government on Earth is...the one product that's so ubiquitous...it’s used by almost everyone in the world on a daily or even hourly basis: money.

ReplyDeleteSo should this conventional policy that's existed for over 100 years now be continued, considering these are unconventional times with the East planning it's own monopoly?

https://www.youtube.com/watch?v=x0A154ALdbE

To be sure, I hold no expectation that private money would lead to a perfect world where there are no crises or problems, just a better world. Better not just in a strictly utilitarian sense but also in a moral sense, as people could store the fruits of their labor however they see fit and not be forced to submit to a tax (inflation) that is not explicitly levied and voted on.

I think inflation, if it is generated by the policies of government, IS explicitly levied and voted on, actually. It is externally-generated inflation that is not - for example, the inflation arising from oil price rises.

DeleteTo be discussing the nature of money on a post about the dire situation of a member of the Eurozone is simply priceless. The monopoly nature of the Euro and its inadequate construction IS the problem. Unfortunately it is not so easy to abandon as the Gold Standard.

There are already other forms of money in existence that are widely used, notably in developing countries. No-one is preventing their use, and they are already diluting the effectiveness of monetary policy. Again, I have discussed this elsewhere:

http://coppolacomment.blogspot.co.uk/2012/07/the-nature-of-money.html

How can you say that spending money on destruction produced a healthy recovery? What about all the poor soldiers, and their children? What about the grieving families and all the sorry politicians? Are you seriously saying, Frances, that you think the cumulative effect of all that misery was progressive?

ReplyDeleteIt sounds regressive, to my mind at least, for the principal purpose of commerce is to grow things, not to take us back in time by killing people and destroying property.

You wouldn’t argue against that, would you? I certainly hope not!

What if the West weakened itself precisely because it relied on the sentiment you just so eloquently outlined - the delusional belief that forcing people to hate each other can create a world you yourself, and your family and friends want to see you? Surely not!

Perhaps you may wish to think about:

THE DUNNING-KRUGER EFFECT: http://www.abc.net.au/radionational/programs/scienceshow/the-dunning-kruger-effect/3102360

"Whenever you find yourself on the side of the majority, it is time to pause and reflect." - Mark Twain

You are missing the point. It took a major war to persuade politicians to provide the public spending that was needed to counteract the private sector debt deflation. And yes, it did produce a healthy recovery. But the point is that spending at that level much earlier on WITHOUT a major war would also have generated a healthy recovery, and without the appalling damage to people's lives caused by both the war and the preceding depression.

DeleteIf you had actually read my post on the US (I gave you the link) you would have seen that I made EXACTLY that point. I do not recommend war: on the contrary, I think it is very sad that only war generated the political will for the level of public spending required to end the Depression.

It sounds as if you believe that, if necessary, its okay for employees of a central bank to launch giant wars killing millions of people "to end the Depression". Clearly, then, I simply cannot offer you anymore ideas, except to say you probably should very seriously consider not just this interview but also the corresponding book, because I suspect your refusing to acknowledge common sense is stemming from some overly-confident faith in God produced by your Christianity.

ReplyDeleteDivinity of Doubt

https://www.youtube.com/watch?v=CmvYyr7cAik

Last comment from me, Frances, Peace out :-)

This is utter nonsense. You are wilfully misinterpreting what I said. I have never, ever suggested it was "ok for employees of a central bank employees to launch giant wars". (Not that they ever have done, of course). I said that the level of public spending required to end the Depression was not provided until WWII. And I specifically said that it was very sad that it took a war to generate the political will to provide the necessary level of public spending to end the Depression. That is NOT, emphatically NOT, suggesting that war is justified on economic grounds. I would not ever suggest such a thing.

DeleteI'm quite happy for you to stop commenting here. You are using my blog to promote your own agenda that you wish to promote, and you are not willing to read what I say properly. You deliberately misinterpret what I have said and now you attack my beliefs as well. I don't want to hear from you again.

Putting side technical complexities too complicated to go into here, he's right insofar as central banks have financed wars; the BBC produced this documentary based on the historical record showing how numerous US and UK central bankers financed Hitler, for example.

ReplyDeleteBanking With Hitler

http://www.youtube.com/watch?v=YauM5dHLn1s

It's fairly amazing, really, that the British civil "servant" who ridiculed US elites for not wanting to profit from dealings with the Nazis during the worst war in human history...left such a blatant paper trail all over the place...

ReplyDeletehttp://en.wikipedia.org/wiki/Edward_Playfair

This sums up your debate perfectly:

ReplyDeleteLord Acton & Polycentric Legal Orders

https://www.youtube.com/watch?v=JA7keww37j0