UK inflation and the oil price

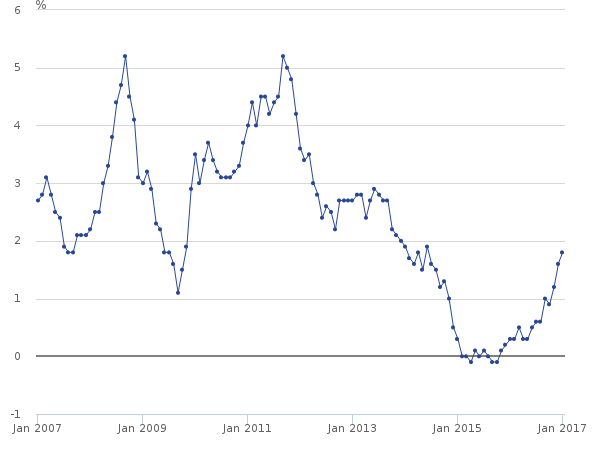

Inflation is back. Here is the change in the consumer price index (CPI) for January 2017, according to ONS : Well, this doesn't look too serious. CPI is barely reaching the Bank of England's target of 2%. It has been much higher for most of the last decade, and yet the Bank of England has kept interest rates at historic lows. But consumer price inflation - the prices that people pay for goods in the shops - is only one side of the equation. On the other side is producer price inflation (PPI), the prices that companies pay for the materials and energy they need to produce goods and services. The picture here is entirely different, as this table from ONS's January 2017 producer price inflation report shows: Annualised producer price inflation has risen dramatically in the last six months. It reached double digits in October 2016 and currently stands at an astonishing 20.5%. Most of that is due to sharply rising import prices, of which by far the most important ...