The dominance of Brexit

Some people have been saying that sterling's fall has nothing to do with the Brexit vote. Sterling was already falling before the vote, they say, because of the UK's wide and growing current account deficit. So I thought I would fact check this.

Here is the UK's current account deficit since 1987, courtesy of ONS:

Well, ok, it has rarely been anywhere near balance in the current century, and it has been trending downwards since 2011.

Now let's look at sterling. Here is sterling's trade-weighted exchange rate since 1992, courtesy of the Bank of England (via this House of Commons briefing paper):

Umm. The correlation between the current account deficit and the trade-weighted value of sterling appears to be negative. Sterling has been rising since 2011 - until this year.

This is actually reasonable. The trade-weighted value of a currency reflects the external performance of the economy. And for a long time now, current account deficits have not been regarded as important for countries with floating exchange rates and independent central banks. So sterling has risen because the UK has been doing well compared to other countries - notably the depressed EU.

Breaking down the current account into its component parts shows why the current account and the value of sterling have been negatively correlated. Broadly speaking, the current account is made up of the goods and services trade balance, plus net investment income. The second of these is the income that UK investors earn from their investments abroad minus the income that foreign investors earn on their investments in the UK.

This is what has happened to net investment income (this chart from ONS also includes other financial income, but net investment income is by far the largest component for the UK):

In days gone by, higher rates of return would have reflected higher risk and would therefore have been accompanied by a lower currency exchange rate. But we live in strange times. These days, depressed economies such as the Eurozone have low rates of return, partly due to central bank action and partly due to a generally poor economic outlook. Higher rates of return accompanied by increased FDI indicate relative economic strength. The negative net investment income position is thus a net positive factor for the UK economy, and until recently this was reflected in the rising value of sterling. Thus the negative correlation of current account and sterling exchange rate is not a bug, it is a feature arising from the peculiar construction of the UK's current account - which in turn reflects the UK's position as one of the world's premier financial centres.

ONS shows that the trade balance (goods and services) has been pretty stable, though negative, for the whole of this century:

We do see some positive correlation between the trade deficit and the value of sterling, though we can't tell from these charts whether sterling responds to the trade deficit or vice versa - or whether both are responding to something else. But this relationship is dwarfed by the negative correlation of the net investment income balance and the external value of sterling. Basically, people like investing in the UK.

Or they used to. This is what has happened to sterling recently:

This chart could be interpreted as showing a downward trend since the mid-2014 peak. But in fact it is showing reversion to previous levels from the mid-2014 peak, followed by three abrupt falls, one at the beginning of 2016, a larger one in June and a third that has not yet bottomed out. The first of these was due to the market turbulence and worries about bank profitability at the beginning of 2016. But the other two are unquestionably due to the Brexit vote.

The fall of sterling from the beginning of 2016 is even more obvious in the sterling-euro exchange rate:

Sterling rose immediately prior to the EU referendum because of opinion polls suggesting that Remain would win. As the referendum result was announced, it fell sharply against both the US dollar and the euro. Although it stabilised in the summer, it has not recovered from this fall.

A second fall was recently triggered by comments by the Prime Minister, Theresa May, at the Conservative party conference, and the growing likelihood that Britain will leave the EU in the most economically damaging manner possible - a "hard Brexit". Financial markets are particularly concerned at the prospective loss of "passporting rights" to the EU. The UK's position as the world's premier financial centre is under serious threat - and this is reflected in the falling exchange rate of sterling.

And not just in the sterling exchange rate. Gilts are affected too, as this Reuters chart shows:

After the Brexit vote, gilt yields fell as output forecasts for the UK were slashed and a Bank of England interest rate was priced in. Remember we live in strange times: cutting interest rates is now a negative indicator for an economy, whereas in the inflationary 1970s and 1980s (and indeed in countries such as Russia where inflation has been very high in recent years) it was a positive one.

So used are we to the weirdness of low interest rates that we have forgotten how normal risk pricing works. But we are now being reminded. As it became ever clearer that the UK government was contemplating a hard Brexit, gilt yields started to rise. Now, sterling is falling as well. This is what capital flight looks like in a country that issues its own currency.

Last time we saw capital flight in an advanced economy was the Greek crisis last summer. Everyone remembers Greek bond yields spiking and Target2 imbalances growing as investors and depositors fled from the prospect of Grexit. But there was no currency component to that (well, there was, but you wouldn't find any charts showing the sharply falling implied exchange rate between euros in Greek banks and euros everywhere else). Now, we have capital flight from another advanced country - and this time it is reflected not only in rising yields but in a falling exchange rate. The UK has become a risky place for investors.

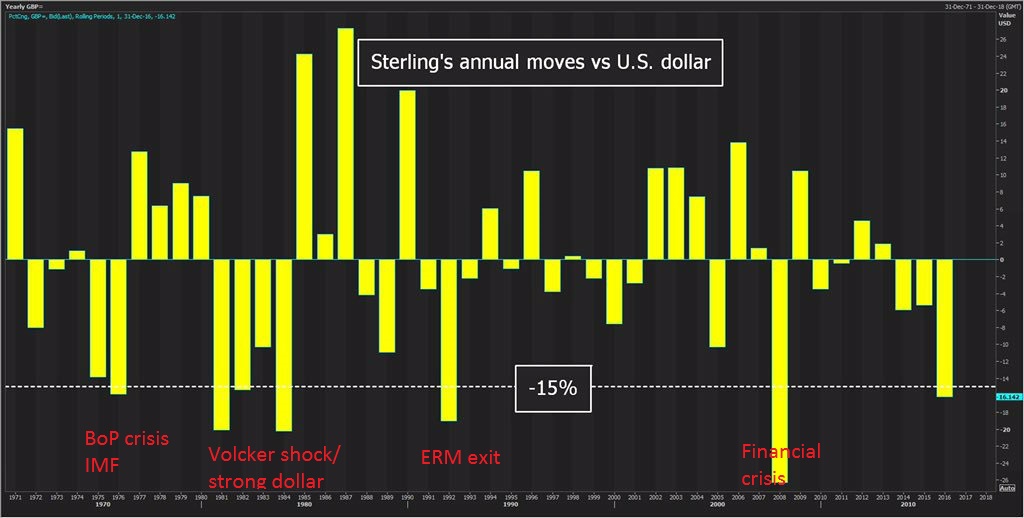

Of course, this might only be a short-term effect. The UK government and the EU authorities are both considering their options at the moment, and once the form that Brexit will take becomes clear and the path defined, both sterling and gilts may well bounce back. Sterling has had larger falls than this, and always bounced back:

But there is, of course, the elephant in the room. All of the sterling shocks in this chart occurred during Britain's membership of what started as the EEC and later became the EU. Indeed, the UK has been a member of the European Union project for the whole of its recent experiment with fully floating exchange rates, which started in 1979 with the lifting of exchange controls. To what extent has EU membership helped to stabilise sterling's exchange rate - and does it now face a more turbulent future? We do not know.

Recently, some have expressed concern about the UK's dependence on external investors - what Mark Carney, quoting Tennessee Williams, called "the kindness of strangers". This is because the UK has both a current account deficit and a fiscal deficit: if both deficits are dependent on external financing, a "sudden stop" can force a very sharp fiscal adjustment and a rapid, highly damaging fall in GDP. There is an outside chance that the current combination of falling currency and rising gilt yields could be the start of a "sudden stop". However, the Bank of England's staff blog recently looked at the financing of the UK's twin deficits and concluded that the fiscal deficit, at any rate, was largely domestically financed so was not in any immediate danger. The current account deficit of course could be subject to a wrenching adjustment if investors fled, although FDI generally tends to be fairly stable. But the two deficits are largely separately financed, so there is little danger of the sort of toxic feedback loop that can ultimately lead to economic collapse and debt default.

What does seem likely is that the net interest income deficit will close, not because returns for UK investors in foreign assets improve but because returns for foreign investors in the UK will now fall due to lower interest rates, QE and a poorer growth outlook. FDI, too, seems likely to decline, though perhaps gradually. No doubt those who are obsessed with current accounts will cheer as the net interest income deficit shrinks, but I wouldn't regard this form of rebalancing as positive, personally. I'd much rather see net investment income turn positive due to higher returns to UK investors from improved growth in Europe.

And what about that trade deficit in goods and services? Well, that might shrink too. Exports will be flattered a bit by the lower exchange rate, and higher inflation will force UK households and businesses to cut back spending, reducing imports. But in the longer term, the outlook for the trade balance depends on what sort of trade deals the UK can cut.

And that brings me back to where I started. Those who thought the fall in sterling was due to a widening current account deficit have the causation wrong. The current fall in sterling is entirely due to Brexit. And the current account deficit is likely to close because of the effect of Brexit on trade and investment. Brexit will determine the behaviour of every UK metric for the foreseeable future.

Related reading:

Short-run effects of the Brexit shock

The currency effects of Brexit

Here is the UK's current account deficit since 1987, courtesy of ONS:

Well, ok, it has rarely been anywhere near balance in the current century, and it has been trending downwards since 2011.

Now let's look at sterling. Here is sterling's trade-weighted exchange rate since 1992, courtesy of the Bank of England (via this House of Commons briefing paper):

Umm. The correlation between the current account deficit and the trade-weighted value of sterling appears to be negative. Sterling has been rising since 2011 - until this year.

This is actually reasonable. The trade-weighted value of a currency reflects the external performance of the economy. And for a long time now, current account deficits have not been regarded as important for countries with floating exchange rates and independent central banks. So sterling has risen because the UK has been doing well compared to other countries - notably the depressed EU.

Breaking down the current account into its component parts shows why the current account and the value of sterling have been negatively correlated. Broadly speaking, the current account is made up of the goods and services trade balance, plus net investment income. The second of these is the income that UK investors earn from their investments abroad minus the income that foreign investors earn on their investments in the UK.

This is what has happened to net investment income (this chart from ONS also includes other financial income, but net investment income is by far the largest component for the UK):

As ONS explains, the fall in net investment income is driven by two factors:

- rising FDI into the UK from 2011 onwards

- higher rates of return on foreign holdings of UK assets than on UK holdings of foreign assets

This chart shows these effects clearly:

ONS shows that the trade balance (goods and services) has been pretty stable, though negative, for the whole of this century:

We do see some positive correlation between the trade deficit and the value of sterling, though we can't tell from these charts whether sterling responds to the trade deficit or vice versa - or whether both are responding to something else. But this relationship is dwarfed by the negative correlation of the net investment income balance and the external value of sterling. Basically, people like investing in the UK.

Or they used to. This is what has happened to sterling recently:

This chart could be interpreted as showing a downward trend since the mid-2014 peak. But in fact it is showing reversion to previous levels from the mid-2014 peak, followed by three abrupt falls, one at the beginning of 2016, a larger one in June and a third that has not yet bottomed out. The first of these was due to the market turbulence and worries about bank profitability at the beginning of 2016. But the other two are unquestionably due to the Brexit vote.

The fall of sterling from the beginning of 2016 is even more obvious in the sterling-euro exchange rate:

Sterling rose immediately prior to the EU referendum because of opinion polls suggesting that Remain would win. As the referendum result was announced, it fell sharply against both the US dollar and the euro. Although it stabilised in the summer, it has not recovered from this fall.

A second fall was recently triggered by comments by the Prime Minister, Theresa May, at the Conservative party conference, and the growing likelihood that Britain will leave the EU in the most economically damaging manner possible - a "hard Brexit". Financial markets are particularly concerned at the prospective loss of "passporting rights" to the EU. The UK's position as the world's premier financial centre is under serious threat - and this is reflected in the falling exchange rate of sterling.

And not just in the sterling exchange rate. Gilts are affected too, as this Reuters chart shows:

After the Brexit vote, gilt yields fell as output forecasts for the UK were slashed and a Bank of England interest rate was priced in. Remember we live in strange times: cutting interest rates is now a negative indicator for an economy, whereas in the inflationary 1970s and 1980s (and indeed in countries such as Russia where inflation has been very high in recent years) it was a positive one.

So used are we to the weirdness of low interest rates that we have forgotten how normal risk pricing works. But we are now being reminded. As it became ever clearer that the UK government was contemplating a hard Brexit, gilt yields started to rise. Now, sterling is falling as well. This is what capital flight looks like in a country that issues its own currency.

Last time we saw capital flight in an advanced economy was the Greek crisis last summer. Everyone remembers Greek bond yields spiking and Target2 imbalances growing as investors and depositors fled from the prospect of Grexit. But there was no currency component to that (well, there was, but you wouldn't find any charts showing the sharply falling implied exchange rate between euros in Greek banks and euros everywhere else). Now, we have capital flight from another advanced country - and this time it is reflected not only in rising yields but in a falling exchange rate. The UK has become a risky place for investors.

Of course, this might only be a short-term effect. The UK government and the EU authorities are both considering their options at the moment, and once the form that Brexit will take becomes clear and the path defined, both sterling and gilts may well bounce back. Sterling has had larger falls than this, and always bounced back:

But there is, of course, the elephant in the room. All of the sterling shocks in this chart occurred during Britain's membership of what started as the EEC and later became the EU. Indeed, the UK has been a member of the European Union project for the whole of its recent experiment with fully floating exchange rates, which started in 1979 with the lifting of exchange controls. To what extent has EU membership helped to stabilise sterling's exchange rate - and does it now face a more turbulent future? We do not know.

Recently, some have expressed concern about the UK's dependence on external investors - what Mark Carney, quoting Tennessee Williams, called "the kindness of strangers". This is because the UK has both a current account deficit and a fiscal deficit: if both deficits are dependent on external financing, a "sudden stop" can force a very sharp fiscal adjustment and a rapid, highly damaging fall in GDP. There is an outside chance that the current combination of falling currency and rising gilt yields could be the start of a "sudden stop". However, the Bank of England's staff blog recently looked at the financing of the UK's twin deficits and concluded that the fiscal deficit, at any rate, was largely domestically financed so was not in any immediate danger. The current account deficit of course could be subject to a wrenching adjustment if investors fled, although FDI generally tends to be fairly stable. But the two deficits are largely separately financed, so there is little danger of the sort of toxic feedback loop that can ultimately lead to economic collapse and debt default.

What does seem likely is that the net interest income deficit will close, not because returns for UK investors in foreign assets improve but because returns for foreign investors in the UK will now fall due to lower interest rates, QE and a poorer growth outlook. FDI, too, seems likely to decline, though perhaps gradually. No doubt those who are obsessed with current accounts will cheer as the net interest income deficit shrinks, but I wouldn't regard this form of rebalancing as positive, personally. I'd much rather see net investment income turn positive due to higher returns to UK investors from improved growth in Europe.

And what about that trade deficit in goods and services? Well, that might shrink too. Exports will be flattered a bit by the lower exchange rate, and higher inflation will force UK households and businesses to cut back spending, reducing imports. But in the longer term, the outlook for the trade balance depends on what sort of trade deals the UK can cut.

And that brings me back to where I started. Those who thought the fall in sterling was due to a widening current account deficit have the causation wrong. The current fall in sterling is entirely due to Brexit. And the current account deficit is likely to close because of the effect of Brexit on trade and investment. Brexit will determine the behaviour of every UK metric for the foreseeable future.

Related reading:

Short-run effects of the Brexit shock

The currency effects of Brexit

A quibble. Returns for UK investors in foreign assets will improve to a degree, simply because of the effect of sterling devaluation on dollar and euro-denominated assets. Also, if the fall in the pound leads to higher inflation, this may prompt an increase in interest rates and thus help prop up sterling transfers to foreign investors.

ReplyDeleteYes, that's a good point, though I was assuming that sterling would stabilise and the current account would slowly close. At the moment, because of currency effects, it is actually widening, of course.

DeleteSignals from the BoE so far indicate that they have no intention of raising rates. I suspect that any signal that they were even considering such action would send sterling off a cliff, unless inflation were far higher than it is now. We are not in the 1970s.

I think you're right that the BoE will be very reluctant to raise rates, but they're going to face increased political pressure to do so; and not just from the usual suspects, but from domestic savers who imagined (however illogically) that Brexit would return them to happier days.

DeleteGiven the recent antipathy towards "cosmopolitans", it will be interesting to see if the BoE is accused of favouring "disloyal" UK owners of foreign assets.

Strewth, that was quick ...

Deletehttp://www.telegraph.co.uk/news/2016/10/17/central-bankers-have-collectively-lost-the-plot-they-must-raise/

William Hague has lost the plot. If central banks raise interest rates because politicians threaten to take away their independence if they don't, they are no longer independent. No way should the world's central banks give in to this. Raising interest rates to please voters when the economic situation doesn't justify it is a bad way to run the economy.

DeleteInteresting but also contentious, Frances. Quite a few more points than I initially expected to note (apologies):

ReplyDelete1. Most of the SHOCK! decline in “the pound” is in Cable. In EUR terms the GBP is simply back to around where it was in the early teens after rocketing away over 2013-2015. This contrast tells us as much about USD:EUR strength as it does “Brexit”-induced weakness in sterling.

2. The assertion “And for a long time now, current account deficits have not been regarded as important for countries with floating exchange rates and independent central banks.” is just that, an assertion, and a constructively ambiguous one. “Not been regarded as important” by whom and when and for what? Is a persistently large C/A deficit “not important” to the trade-weighted value of a currency? Is it “not important” in what it tells us about the underlying performance of an economy? You’ve presented good evidence of a negative correlation for the UK “since 2011”, but is that conclusive? It seems presumptive to dismiss a complicated economic relationship out of hand on the basis of a short-run absence of positive correlation.

3. Similarly: “The trade-weighted value of a currency reflects the external performance of the economy.” Or does it reflect relative expectations on interest rate differentials? Part of the problem here – and not of your creation, obviously – is that FX movements aren’t always driven by consistent factors, particularly in the short-term. There’s a reasonable argument that the recent move in Cable is due to the UK monetary outlook shifting (admittedly abruptly/unexpectedly) from “hiking” to “lower for longer” versus continued relative expectations for the US of “hiking”. This shift in expectation would be, obviously, Brexit-influenced but, as I said before (in relation to GBP:EUR), doesn’t tell the whole story.

4. I think you’ve highlighted a very important aspect of the C/A deficit’s growth, i.e. net investment income. However, I wonder if there’s a compositional element that’s important in the UK’s foreign assets and liabilities. Why have the UK’s foreign assets seen so much larger a decline in rate of return than foreign liabilities? You attribute this to a weak Eurozone, but the UK invests globally (i.e. not just in the EU) and prevailing yields in the UK have also plummeted over the period. This gap in relative returns is not well-explained at all, so I don’t think there’s much basis for your conclusion that “The negative net investment income position is thus a net positive factor for the UK economy…” Additionally, rising FDI may indicate “relative economic strength”, but it may also indicate foreign participation in UK asset bubbles and/or money laundering of exported capital. Again, I don’t think there’s a good basis to conclude that it’s evidence of a “strong” UK economy.

5. The other compositional factor that you leave out is that persistently large C/A deficits have to be “funded” with capital flows, e.g. via FDI, thus there is a self-reinforcing aspect to the UK’s C/A deficit that is important and this is visible in the “position” size of UK foreign liabilities growing far more rapidly than UK foreign assets.

6. The recent rise in UK bond yields seems to correlate with that in US bond yields. Was the rise in US bond yields “Brexit”-driven? Unlikely, so it makes it less likely that the rise in UK bond yields is solely “Brexit”-driven.

7. Capital flight? Seriously? We’ve seen large price moves in both the GBP and gilts in recent history without there being much evidence of UK capital flight or flood. Why reach for hyperbole?

8. “The UK's position as the world's premier financial centre is under serious threat - and this is reflected in the falling exchange rate of sterling.” Umm. London was the world’s premier financial centre for centuries before the EU existed. It was Europe’s financial centre WHILE the EEC existed AND didn’t include the UK. “Hard Brexit” may well prove to be damaging to the City but I think you’re reaching for hyperbole.

These are interesting comments in response to a masterful blog (for which many thanks). As to London's enduring status as a pre-eminent financial centre, I am not so sure: Genoa, Florence, Augsburg, Antwerp, Amsterdam, etc., have held the palm at various times, and scarcely anyone doubted that their importance would cease - until it did (see, for instance, Y. Cassis 'Capitals of Capital: a History of International Financial Centres, 1780-2005' (CUP, 2006)).

DeleteIt is sometimes forgotten that the City had become a comparative backwater by the 1950s. Its revival was made possible, in part, by virtue of the actions of foreign countries: Regulation Q, the US interest equalisation tax of 1963, the development of the Eurodollar (and, later, Eurobond) markets in response to restrictions on Soviet currency trading in the New York, etc. Then the City - though perhaps not much of the country - benefited from the opportunistic kindness of strangers. This time around the City could well lose a measure (or, indeed, much) of its prestige and affluence on account of the antipathy of strangers (via the removal of passporting amongst other sanctions). The City might then join Augsburg or Amsterdam in the long list of faded entrepots.

I recall that it was Blanche DuBois who noted how she had "always depended upon the kindness of strangers". It didn't end too well for her, as I suspect Mr Carney knew all too well when he recycled that quotation.

Just found your blog, great info, you got yourself a new follower :)

ReplyDeleteDon't seem to be able to reply directly to Froghole above, so posting a separate comment - sorry.

ReplyDeleteFair point, Froghole – “Look on my banks, ye Mighty, and despair!” yada yada.

However. All financial centres were “comparative backwaters” in the 1950s relative to previous and succeeding eras. Recent events had put something of a dent in international finance.

Of the historical financial centres you mention, none existed in a “regionalised”, let alone “globalised” financial system as we understand it today. Genoa and Florence financed their respective mercantile empires, the Fuggers of Augsburg intermediated for the Habsburgs, as did Antwerp. It’s necessary to fast-forward to Amsterdam before we see the beginnings of globalisation as we know it and, again, the history is of new centres supplanting old on the basis of mercantile supremacy – rounding the Cape meant that the Dutch (and others) broke forever the trading dominance of the Mediterranean. That pattern was followed by London’s rise as the English mercantile empire supplanted the Dutch in the 18th century but, curiously, the pattern then broke: New York rose to dominate the USA, but not Europe or the world. London continues to dominate finance despite the UK economy’s inexorable slide into relative irrelevance.

The era of globalisation, which we’re still in, concentrates financial skills and resources in regional centres grouped by time-zone and that concentration is self-reinforcing in a manner reminiscent of natural monopolies. New York does huge business in Latin America despite the USA not being part of an EU-like SuperAmerica. Hong Kong and Singapore do business throughout Asia on the same basis. London is it for the European region/time-zone, within or without the EU, and any regional rival would need to supplant it. Frankfurt’s bucolic toy-town won’t cut it. Paris? Maybe, but for the French. Amsterdam? Again: fuggerdaboudit. It’s easy for London, a quasi-citystate, to be paranoid about losing its privileged position until you line up the competition. Then the debate just looks daft.