About those UK CPI inflation figures....

The UK's CPI inflation figure for October 2012 rose by 0.5% to 2.7%. A small rise had been predicted, but this was much larger than expected. The ONS attributed the rise to increases in tuition fees, food and transport costs. I shall discuss the implications of these components shortly.

Not surprisingly, the inflation hawks were out in force. Market Oracle led with a "shock, horror" headline:

Not surprisingly, the inflation hawks were out in force. Market Oracle led with a "shock, horror" headline:

UK CPI Inflation Soars Despite Bank of England Deflation Propaganda, Shocks Academic EconomistsAnd they showed this chart as evidence of what they called an "inflation mega-trend":

(for larger version, click here)

And Andrew Sentance, in a news release from Price Waterhouse Coopers, made the following pessimistic prognosis:

"UK inflation remains stubbornly above the 2% target. And with further energy and food price rises in the pipeline, it could rise further in the coming months. This would reinforce the squeeze on UK consumers and add to concerns about the Bank of England's ability to achieve its price stability objective. If above target inflation persists through next year, it will add to the pressure on the MPC to raise interest rates sooner rather than later."

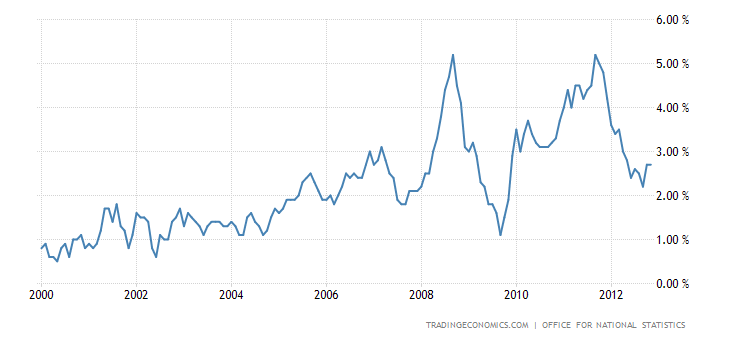

Well, his first statement is correct. UK inflation has remained stubbornly above 2% since 2010. But this chart from Trading Economics shows that in fact it has been above 2% on average since 2005:

(for larger version, click here)

So given that, what on earth is the tearing hurry to bring it down to 2%?

Now, I will admit that this chart does show that there has been high inflation in the last two years - as indeed there was in the run-up to the financial crisis (really the BoE should have been paying more attention to the trend!). But since the peak of 5.2% in October 2011 the trend has been sharply downwards. In fact CPI inflation has been falling nearly as sharply as it did in 2009. Yes, there have been a couple of spikes, but there is no doubt that the underlying trend for the last year (at the time of writing) has been deflationary.

There are two possible ways of viewing the current spike. One is that it is just that - a spike - which will not affect the overall downward trend. If this is correct, then we should expect CPI inflation to fall again in November or December. In support of this argument, the ONS notes that of the 0.5% rise in CPI, 0.3% is due to a substantial increase in student tuition fees that has just come into force: this would unwind itself in due course. And as it also does not affect "ordinary" consumers, it is arguably a distortion. That leaves an increase of 0.2% due to externally-driven food and fuel rises partially offset by price falls in other sectors. If price-cutting continues in other sectors, CPI inflation may well return to trend even if world commodity prices continue to rise.

The alternative view is that this increase in CPI is a trend reversal - that the September figure was the turning point and this is the start of a rising trend in CPI inflation similar to that in 2010. This is clearly Sentance's view and it may also have been the reason for the MPC's decision to end the QE programme. Clearly the 0.3% rise due to tuition fees cannot be regarded as a trend reversal, since it is a one-off change. However, Sentance is probably correct that food and fuel will continue to rise in price, because the world price of essential foodstuffs is rising due to drought affecting supply, and the oil price is also rising due to world economic conditions. Furthermore, utility bills are expected to rise substantially in the next few months. If this is a trend reversal, price-cutting in other sectors will not be enough to offset inflation in these key sectors.

So it is by no means clear what the direction of CPI inflation will be over the next few months. What is clear, however, is that this month's CPI inflation increase is not due to pressure from a growing domestic economy. Here's the UK's GDP growth rate since 2008:

(for larger version, click here)

In the last quarter, the UK economy managed to grow by a measly 1%. Inflationary growth? Hardly. No, the CPI inflation increase is due to Government policy (the tuition fees increase) and external factors (rising price of commodities). So despite Sentance's gloomy prognosis, raising interest rates would not help. In fact it may make things worse. Many households and businesses are interest rate sensitive at the moment: a 50bps rise in the base rate, at a time when real incomes are falling, would increase the level of serious financial distress, with consequent impact on business production and consumer spending. Really it would not be clever to try to choke off a possible inflation trend reversal at the price of UK economic growth.

The Bank of England should hold its nerve and continue to support economic growth. Even if this is a trend reversal, inflation really is not the main issue at the moment.

{kind=link}

{kind=link}

{kind=link}

Isn't it a problem in relation to wage growth, I.e., without matching wage growth household debt becomes less serviceable. Not an argument for interest rate rises of course.

ReplyDeleteReal incomes are falling because of inflation, so no chance of economic growth while that continues. Thanks BoE....

ReplyDeleteFrances,

ReplyDeleteThe whole idea of "raising interest rates" is increasingly passé; economies are moving to free(er) (interest) rates; determined more 'arbitrarily' by more opaque markets with less discernable boards of particular men to whom participants can look towards for clues as to the next 'move'. I repeat, once again, global capital markets are the principal drivers of economic activity. Government employees - be them central bank officials or not - are periphery in this context.

Frances, I am a (recent) big fan of your blog. Well done (!!). In my opinion, you are one of the few financial blogs worth reading on the entire Net. You are an excellent observer of many things financial (especially in regard to the world of banking) and I do certainly hesitate to criticize. However, as someone who lives off his investments and is a keen full-time observer of all things economic and financial, I must point out that your comments today regarding the "rising price of commodities" are not sufficiently defined well enough (or backed by the actual data). In which time frame are you describing this "rise"? Please check the CRB Index chart over the last 12 months -- no significant rise in price (it has fallen). Then check the DBA (the NY ETF for Agricultural Products)--- again, no significant rise over 12 months. Then the DBB (the NY ETF for Metals) -- again, no significant rise over 12 months. Then the price of Oil -- again, no significant rise over 12 months (in fact, there has been a significant drop). Then the price of Copper -- again, no significant rise over 12 months. Then Natural Gas -- again, no significant rise over 12 months. Wheat and Corn over 12 months -- yes, there seems to have been a rise (but to my eye those prices appear to now be moving back down again). Sugar -- price has fallen significantly over the last 12 months. Iron Ore -- price has fallen significantly over the last 12 months. All forms of steel -- price has fallen significantly over the last 12 months. Coal (the ETF in NY is KOL) -- price has fallen significantly over the last 12 months. Uranium (the ETF in NY is NLR) -- price has fallen significantly over the last 12 months. Admittedly, some of those ETF's are derivatives and not actual commodity prices. However, over time, I find that they generally reflect more accurately what is really happening in their various commodities and related industries. And the actual commodity prices I refer to speak for themselves. So ........... there is deflation and inflation occurring at the same time. But in the long run, prices of the key economic inputs to most advanced western economies (including wages) appear to be steadily deflating since the beginning of the global banking crisis in 2008. And this trend seems to be gathering pace since early 2011 and especially over the last few months of 2012. What HAS been inflating in many crisis affected western economies is the base money supply since 2008, thanks to QE from negligent central bankers but that has not been enough to trigger any significant recovery in private credit expansion. Because QE increases the "financialization" of an economy, it feeds through to increased costs of services. Meanwhile, the real economy involving goods is contracting and deflating. Soon the services economy will (probably) follow. Government austerity policies should speed that process. Then the crisis in private pension funding caused by inadequate investment returns will hit with full force. The half life for that (horrendous crisis yet to come) is about 5 years -- so a good guess is that it should start somewhere within the next 12 - 18 months. I would suggest keeping the seat belt fastened -- tightly. My key point, however, is that inflation and deflation are highly complex issues of relativity. Too many economists and financial commentators simply don't understand the basics of price dynamics. Modern economic theory has misled them into believing that prices are related to demand and supply generated from "rational" human beings. Please take my criticism here as constructive. You are simply one of the best commentators on banking and I look forward to everything you write on that subject -- congratulations.

ReplyDeleteAverage price of Brent crude has risen from $79.80/barrel in 2010 to $111.61/barrel in 2012. Average price of WTI has risen from $79.40/barrel in 2010 to $94.51/barrel in 2012. EIA projects Brent falling to $103.38 and WTI to $88.29 in 2013, which is consistent with your ETF. But to say oil prices have fallen is simply wrong. They have clearly risen considerably over the last two years.

ReplyDeletehttp://www.eia.gov/forecasts/steo/report/prices.cfm

The US wheat price soared 25% in July due to drought and has not fallen from that level, although there are signs that it is beginning to do so. That is an enormous increase which is feeding through into consumer prices.

http://www.indexmundi.com/commodities/?commodity=wheat

UK consumers have had a very considerable hike in fuel prices over the last two years, and products involving wheat have also risen considerably in price. This is the source of the 0.2% inflation rise in this month's figures. Large increases in UK utility bills have already been announced, which obviously will also tend to increase CPI inflation. So it is entirely possible that CPI inflation will continue to rise, as Sentance suggests.

Having said that, I agree with you about the generally contractionary environment in the world economy. I noted that whether CPI inflation continues to rise depends on the extent to which price-cutting in other areas offsets rises in food, fuel and energy prices. I don't think that counter-cyclical world price rises in certain commodities should dictate UK economic policy. It is the general trend that is important - and as far as I can see that is poor growth and deflation.

All of my references were pointedly to the 12 month period. Not the 2 year period. That is my point -- people should always state the time frame when referring to any trend in prices (but they don't). By countering with 2 year price history, you are exactly correct in a 2 year sense but totally incorrect in a 1 year sense (with the exception of Wheat and Corn -- but we both seem to see those prices now receding from the US drought induced price surge). I don't know why you chose that time frame as a rebuttal. Why not look at 6 months or 3 years? I would always actually prefer to look at multiple Linear Regression analyses over a series of time frames clearly stated but that was beyond the scope of my comment.

ReplyDeleteHowever, when so many commodities are deflating in price over a 12 month time period and so few are inflating, then it seems to me to be simply a matter of quantity. How can the wheat and corn price rises over the last 5 months overwhelm the 12 month falls in so many other input prices? How can you explain the dramatic fall in UK CPI that has occurred throughout 2012? Here, I actually agree with the negligent Mr Bernanke in that I suspect that inflation will not be a big problem for the sick western economies ............. as long as QE does not light the flame of private credit expansion. The negligent central bankers are pretending that they can "fix" the crisis with this policy. But they did not see the banking crisis coming. And they have launched massive unprecedented actions since its arrival -- but that isn't working. They are pushing on a very long piece of string.

Their negligence and incompetence is slowly becoming obvious to even the casual observer.

The sheer size of the excess private credit creation in the USA , the UK and EU which has fueled excess speculation in asset prices over the last 20 years is the problem. Size matters. They cannot see this and hope to fix it with yet more excess private credit creation (!). MMMmmmmmmmmmmmm.

Brent crude has actually risen slightly in the one-year period too - from avg $111.26 to avg $111.61. But the significant rise for these inflation figures was earlier, as petrol companies would have been locked into future prices that unwound in this period. That's why I used the 2-year time horizon rather than the one-year. On that basis, we should start seeing fuel prices levelling off but not falling any time soon.

ReplyDeleteI'm not intending to make a case either for further inflation or for further deflation in this post. I have noted that there are two alternative views of the data. As I said in my previous comment, personally I think the issue is deflation, not inflation, and the total inadequacy of central bankers' and politicians' responses to the situation doesn't bode well for the future.

I completely agree with you that the real issue is the size of the private debt bubble, and the last thing we need is more private debt.

From the FT:

ReplyDelete“Ten ways HMRC checks if you’re cheating”

http://www.ft.com/intl/cms/s/0/0f98bbc0-2db6-11e2-9988-00144feabdc0.html#axzz2CWYjCkXD

I wrote….

This is the corollary viewpoint to not understanding that markets now finance governments, and not vice versa, because the practice of instituting citizens into (legal) existence for the purpose of taxation is increasingly a redundant business model. Boosting taxes will repel capital, while current subjects cannot stand much more taxation. Consequently, central banks will bankrupt themselves (through inflation) while trying to avoid adaptation to this new environment. Darwin himself said that it is not the fastest, the richest or even the strongest that necessarily survive and prosper; it is, rather, the people who are most willing to adapt.

Frances, what are your thoughts on this lecture, by this German economist? It's related.

http://www.youtube.com/watch?v=TBER0noHGC8

Alister,

DeleteIn a fiat currency world it is impossible for markets to finance governments. Banks can, because they have been granted the privilege of creating credit money. But ultimately all fiat currency exists because government says it does. That's what the word "fiat" means. So it is simply nonsense to say that markets finance governments with fiat currency. It's the other way round - governments (usually via banks) provide markets with the fiat currency they need to function smoothly.

I've seen Hoppe's lectures before. I think he's barking.

Frances,

ReplyDeleteImpossible for markets to finance governments? What about capital flight? I know what fiat means - but to suggest that government employees are the single most important pillar upholding global capital markets seems fairly far fetched to me. You would have to be very dedicated to the cause of government force to seriously believe that the current legal tender laws stance any chance of being sustained.

It seems like you overestimate the importance/power/endurance of central banks - it might pay to remember the whole system is built on only some simple illusions previously sustainable only because of a dearth of information. May be worth repeating that yours is not necessarily a very contrarian view in this regard, perhaps even constituting the common norm amongst people, and sometimes the majority can be mistaken, remember, or even act foolishly...

ReplyDeleteExhibit A

http://www.youtube.com/watch?v=Dkv0KCR3Yiw

Perhaps you simply are a cheerleader for the practice of "instituting citizens into (legal) existence for the purpose of taxation". I wonder, do citizens only exist to pay tax? Is there any point to life other than paying tax, according to you? Please, don't respond!

ReplyDeleteDon't worry, Frances, I won't comment here again until at least March, I promise! I feel like I am vandalising your learned space in some ways, knowing that you disagree with me...

ReplyDelete"They issue no binding legislation, but in the banking world, what they say goes"

Applying unwanted force onto people who have not themselves applied unwanted force on anyone else is not sustainable in the 21st century, and not only is it not sustainable, it is simply too costly... Central banks epitomise nationalism, a 20th century phenomenon...Bye for now! :)

http://seekingalpha.com/article/1016161-basel-iii-and-gold

Blah blah. The SeekingAlpha author didn't understand the Basel III rules for Tier-1 gold when he read them. IF he read them.

DeleteThey are quite clear only the amount of physical gold you possess or have allocated to you somewhere, to the extent you also have a liability for the same weight of gold to someone else, will be allowed a 0% risk weighting. All the rest, whether it be physical or paper gold, is 15% weighted. They are quite clear on this.

Probably worth noting that 1 of the particularly influential people with the BIS Supervisors at the moment is Stefan Ingves from Sweden, and Sweden is in the (slow) process of privatising the local government http://www.youtube.com/watch?v=vG51uCrYxVM Food for thought

ReplyDeleteTo the rich-should-pay-more crowd, the question of whether raising taxes hurts economic growth is less important than the issue of "fairness". Why increase taxes on the rich at all? Answer: It's a matter of "fairness." Andy Stern, the former head of the Service Employees International Union, the fastest-growing American union, describes the economic philosophy of the left: If raising taxes on "the rich" hurts the economy, that is an acceptable price. "Western Europe," says Stern, "as much as we used to make fun of it, has made different trade-offs which may have ended with a little more unemployment but a lot more equality."

ReplyDeletehttp://www.jewishworldreview.com/cols/elder112212.php3#.UK30oOPZ_yc

Alister has some potentially valid points...

ReplyDelete"It would open a chink in the armour of sovereign immunity against creditors that countries have largely enjoyed for the past century"

http://www.ft.com/intl/cms/s/0/2b1eb9f0-34d0-11e2-8986-00144feabdc0.html#axzz2CvrfwixN

Government employees adopt debt, ostensibly in the name of their "citizens", without ever actually receiving any direct contractual authority to do so while simultaneously negating any personal responsibility for said debt; they simply assume a magic right to literally sign other people into debt based on some obscure and wholly theoretical state apparatus that is supposedly legitimized by the concept of majority rule.

ReplyDeleteWell, international finance will continue crushing States. Law & order will win the day.

http://www.ft.com/intl/cms/s/0/3bca5b62-34c9-11e2-99df-00144feabdc0.html#axzz2CvrfwixN

. Any court orders that serve to dissuade that type of mischievous should be welcomed with open arms.

It's funny how a prisoner who gets the option to vote on his guard may think that he is free. Johann Wolfgang von Goethe was right when he wrote that...none are more hopelessly enslaved than those who falsely believe that they are free...

ReplyDeletehttp://www.telegraph.co.uk/news/politics/9696815/Prisoners-should-get-the-vote-Lib-Dem-minister-Lord-McNally-says.html

What makes the UK so particularly pernicious is that, unlike Argentina, it ostensibly manages to maintain a patina of respectability. This optical feature of supposed sophistication amongst the owners of UK subjects draws attention away from their intellectual cavities that bankrupted them. No doubt, the UK is in a far worse position than Greece

ReplyDelete