The Great Unemployment Fudge

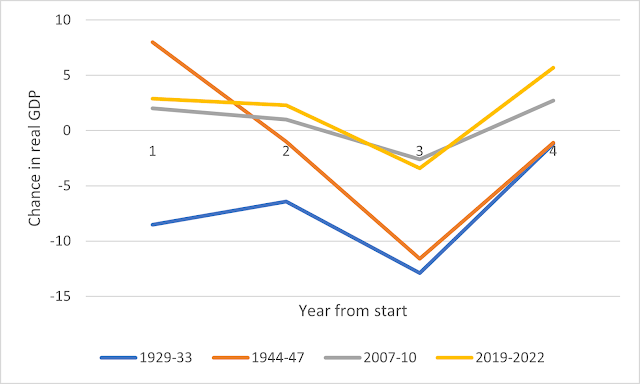

In the U.S., we are told, the post-World War II period was a golden age of full employment. High wartime government spending had brought to an end the double-digit unemployment and misery of the Depression, and as war gave way to peace, unemployment settled at a non-inflationary level of 3-5%. It's known as the post-war "economic miracle". But it's a myth. There was never full employment. The low unemployment of the post-war years is a massive statistical fudge. In fact, over five million people lost their jobs immediately after the end of the war, most of whom never worked again. But they were never listed as unemployed - because they were women. The Great Unemployment Fudge started in the "Depression of 1946", described by the Cato Institute as "one of the most widely predicted events that never happened in American history". During the war, there was full employment, GDP was roaring and industrial production was at an all-time high. But much o...