A tale of two halves

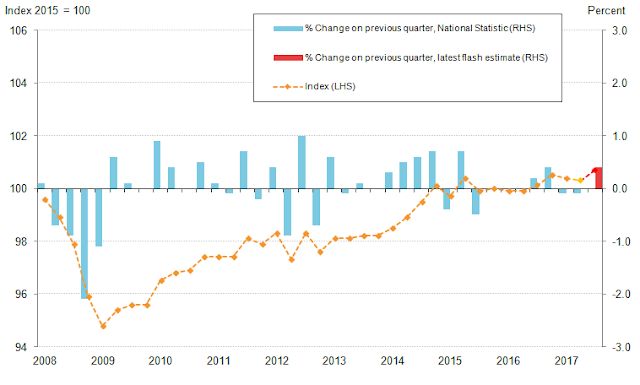

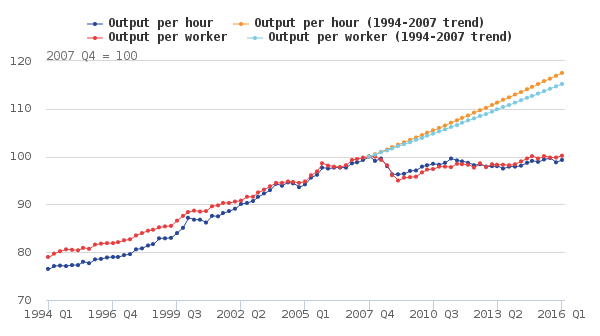

When the banks fell over, they knocked the stuffing out of the British economy. The UK’s productivity has been dismal ever since. Unemployment has fallen to historic lows and wages are rising, but productivity growth remains near zero. This “productivity puzzle,” as it is known, has had economists scratching their heads for best part of a decade. But UK productivity is a tale of two halves. Experimental statistics recently released by the Office for National Statistics (ONS) reveal widely varying productivity levels across the UK. “Productivity grew in half of the 12 regions and countries of the UK in 2018,” says the ONS, “with output per hour increasing in both Scotland and the East Midlands by more than 2%; in contrast, output per hour fell in Yorkshire and The Humber and in Northern Ireland by at least 2%.” It would be easy to ascribe this stark divergence in productivity growth to the dominance of financial services and decline of manufacturing. Financial services are...